Nuclear Power Is No Longer Just the Government’s Game

- 8 min read

- 11,392

- Published 10 Apr 2026

Somewhere in Maharashtra, a factory manager is calculating how many hours of grid power he can count on this month.

Not hoping but calculating.

Because in industrial India, power is not a utility.

It is a planning variable.

Meanwhile, in the background of a busy legislative session, India quietly made a decision that most people missed entirely.

No grand speeches, no dramatic headlines.

Just a policy shift, if it holds, could reshape how this country powers itself for the next fifty years.

For over six decades, since the Atomic Energy Act of 1962, nuclear energy in India sat firmly behind government doors.

It was strategic, sensitive, and tightly controlled, with players like Nuclear Power Corporation of India (NPCIL) doing all the heavy lifting while private capital watched from the outside, curious but unwelcome.

Nuclear power in India followed a simple rule: it stayed within government walls.

Not because capital wasn’t available, but because access wasn’t.

The SHANTI Act doesn’t announce a new direction loudly.

It simply opens a door that was never meant to open.

When a Closed Door Opens, Even Slightly

The Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India (SHANTI) Act changes who gets to participate in nuclear power.

It lets private companies walk into nuclear power, not just as suppliers but as participants across the value chain.

Generation, plant operations, equipment manufacturing, and even joint ventures with public sector firms, all now sit within reach, subject to regulatory approval.

There is even room for up to 49% private or foreign investment in nuclear projects, which quietly aligns India with global norms.

For context, this is not just policy reform, but a mindset shift.

The older framework was written when nuclear power was inseparable from national security.

That world still exists, but it is no longer the only lens.

Energy security, climate commitments, and industrial scale have started demanding a different approach.

And private capital, which once stayed out by design, is now being invited in by necessity.

The Math That Forced the Change

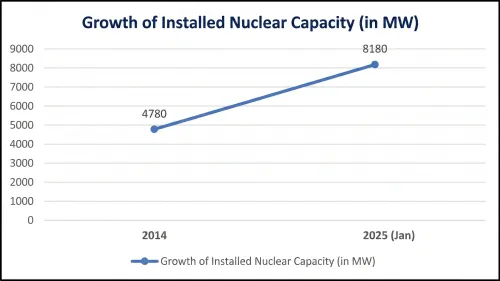

The numbers tell a story that is easier to see than to explain.

Source: Press Information Bureau, Government of India

What that chart shows, stripped of its labels, is a government that has quietly committed to a scale of expansion that public funding alone was never going to support.

India today runs on about 8.8 GW of nuclear capacity.

It is a small slice of a very large power pie, almost easy to overlook when solar parks and wind corridors dominate the headlines.

But the ambition is anything but small.

The targets stretch to 22 GW by 2032, 54 GW by 2047 through existing public sector pipelines, and an overall 100 GW nuclear capacity by 2047.

That is more than a tenfold expansion over two decades.

Now pause and think about what that means in capital terms.

Nuclear plants are not incremental projects.

They are multi-billion-dollar commitments with long gestation periods, complex clearances, and engineering precision that leaves little room for error.

Public funding alone cannot carry that weight.

Which is why the government’s own estimates suggest that nearly 46 GW of future capacity could come from private firms, joint ventures, and state utilities working alongside the public sector.

This is less about choice and more about arithmetic.

If the target is serious, the capital has to follow.

The Technology That Makes It Possible

For years, nuclear expansion was constrained not just by policy but by scale.

Large reactors are expensive, slow to build, and difficult to replicate quickly.

This is where Small Modular Reactors, or SMRs, start to change the conversation.

They are smaller, typically in the 55 to 200 MW range, modular by design, and can be factory-built and assembled on site.

That changes both cost structures and timelines in ways that traditional reactors could not.

India is planning at least five homegrown SMRs by 2033 under a ₹20,000 crore Nuclear Energy Mission.

That number sounds modest until you consider what it enables.

SMRs can be deployed closer to industrial clusters, used for captive consumption, and even placed alongside retiring coal plants.

India’s coal capacity sits at roughly 250 GW, and over time, parts of that base will need cleaner replacements.

SMRs offer a bridge, not theoretical, but practical.

They reuse existing grid connections, leverage known infrastructure, and reduce the friction that usually slows down large-scale energy transitions.

And once that bridge exists, private players have a clearer entry point.

The Names Already Circling the Opportunity

Capital tends to move before clarity becomes consensus.

Early industry assessments suggest India could attract $25–30 billion in private investment over the coming years.

Large conglomerates like Tata Power, Adani Power, Reliance Industries are already being mentioned in that context, though the shape of their participation remains to be defined.

There are also early conversations on the ground.

Adani Group is in talks with the Uttar Pradesh government for up to eight SMRs, translating into about 1.6 GW of capacity.

Sites like Tarapur in Maharashtra and BARC Vizag in Andhra Pradesh are already in focus.

Globally, nuclear has often struggled to attract private capital because of liability concerns.

India faced the same issue under the Civil Liability for Nuclear Damage Act of 2010, where supplier liability made investors cautious.

The new framework softens that friction.

It does not eliminate risk, but it makes participation viable.

And when the regulatory environment becomes workable, capital tends to follow.

Not immediately, but steadily.

Energy, Climate, and the Missing Piece

There is also a deeper reason this shift matters.

India’s per capita electricity consumption is expected to rise sharply from about 1,460 kWh to over 4,000 kWh by 2047.

At the same time, the country has committed to reducing emissions intensity by 45% by 2030 and achieving net-zero by 2070.

Renewables like solar and wind are expanding rapidly, but they come with intermittency.

The sun sets, the wind slows, and grids need stability that does not fluctuate with the weather.

Nuclear power provides that stability.

It is consistent, predictable, and capable of running base-load power without interruption.

Which means this is not just an energy story.

It is a grid story, a climate story, and increasingly, an industrial story.

The Quiet Opportunity in Plain Sight

For investors, the instinct is often to look for direct exposure.

In this case, that path is not obvious yet.

There are no pure-play listed SMR companies in India today.

The operators of tomorrow are still taking shape.

But infrastructure cycles rarely reward only the final operator.

More often, the durable opportunity sits in the ecosystem that builds, supplies, and enables the infrastructure.

Heavy engineering firms, capital goods manufacturers, EPC contractors.

Companies like BHEL, which can manufacture reactor components.

Larsen & Toubro, which already has experience working with NPCIL on nuclear EPC projects.

NTPC, which, given its scale and existing power infrastructure, could be among the earliest non-traditional players to step into nuclear operations.

Then there is the extended supply chain: equipment manufacturing, specialised materials, and long-term service contracts.

Nuclear projects run for decades, and every component becomes part of a recurring economic loop.

This is not a fast cycle. It rarely shows up in a single quarter.

It builds slowly, almost invisibly, and then compounds.

Risks That Do Not Go Away

None of this comes without friction.

Nuclear energy still carries cost disadvantages compared to solar and wind in the current environment.

Land acquisition, regulatory approvals, and supply chain dependencies remain real constraints.

There are also concerns around safety standards if private participation expands without equally strong regulatory oversight.

Liability reforms make investment easier but raise questions about accountability in worst-case scenarios.

These are not small issues; they will shape how quickly the sector evolves.

But they do not change the direction of travel.

A Long Game Disguised as a Policy Update

It is tempting to see the SHANTI Act as just another reform tucked into a busy legislative calendar.

But every now and then, a policy quietly redraws the boundaries of an entire sector.

This feels like one of those moments.

India is not just adding another energy source.

It is opening a previously closed industry to private capital, aligning it with long-term climate goals, and creating a new layer of industrial opportunity that did not exist before.

For investors, this is not a trade, but a theme.

A slow, capital-heavy, regulation-sensitive, decade-long theme where the early signals are easy to miss because they do not look dramatic.

At some point, that factory manager in Maharashtra may stop calculating how many hours of power he can rely on.

Not because demand has changed, but because supply has become more predictable.

And when something as fundamental as power stops being uncertain, entire systems start to behave differently.

The SHANTI Act may read like a policy update today.

But over time, it could quietly change how India builds, powers, and plans its industrial future.

Sources and References:

- THEASIAGROUP

- WORLDNUCLEARNEWS

- LAWASIA

- SANSKRITIIAS

- DRISHTIIAS

- PIB

- NEXTIAS

- REUTERS

The content in this blog is intended purely for educational purposes. Any securities or mutual funds referenced are illustrative in nature and do not constitute a recommendation or endorsement by Kotak Neo. Investors are encouraged to assess their own financial situation and seek professional advice before making any investment decisions. For compliance T&C and disclaimers, Visit https://www.kotakneo.com/disclaimer/

0 people liked this article.