How 5,500 Extra Kilometres Unraveled India's Shrimp Advantage

- 28 min read

- 1,189

- Published 04 May 2026

The Numbers Behind the Shock

India's seafood industry is facing losses estimated between ₹700 crore and ₹1,500 crore due to Red Sea shipping disruptions.

On the ground, Shipping time has increased from 18-20 days to 30-35 days, which is 67% longer than before. Freight costs are up by 30-40%. Around 60% of Europe-bound cargo is now affected. The reason? Ships now have to go all the way around Africa instead of taking the shorter route through the Suez Canal.

To put this in perspective, India exported seafood worth ₹62,408 crore in FY25. The current losses represent 1-2.5% of annual export value. But here's the thing: these losses aren't spread evenly across the year. They're concentrated in a few months, which makes the impact much sharper than these percentages suggest.

How India's Seafood Economy Works

Source: Export volumes and values: Marine Products Export Development Authority (MPEDA) annual reports and monthly trade data

The structure is straightforward.

India's seafood exports are dominated by one product: shrimp, accounting for 70% of export value. When we say shrimp, we're mainly talking about Vannamei, also known as whiteleg shrimp. It's a species originally from Latin America that's now farmed extensively in India because it grows fast, adapts well, and produces the uniform sizes international buyers want.

The production is concentrated geographically. Andhra Pradesh alone produces 47% of India's shrimp, mostly through aquaculture farms. Other coastal states like Gujarat, Tamil Nadu, West Bengal, Kerala, and Maharashtra contribute the rest through a mix of farming and traditional fishing.

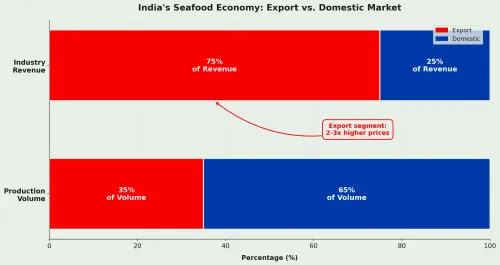

The numbers tell an interesting story: only 35% of India's seafood production by volume gets exported, but that 35% generates 75% of the industry's total revenue. Export prices are 2-3 times higher than domestic prices. A US supermarket pays ₹700-800 per kg for the same shrimp that sells for ₹300-400 per kg in Indian metros. Export buyers pay premium prices for strict quality grading, uniform sizing, certifications, and IQF processing that domestic buyers don't require.

The Industry Was Already Under Stress

Before we get to the current crisis, understand that this industry wasn't in great shape to begin with.

The industry was already dealing with pressure from multiple sides. US tariffs imposed in 2025, ranging from 4.8% to 5.77%, had cut exporter margins by more than half. Feed costs jumped 35-40% between 2022 and 2026. Labour became 40-50% more expensive. Fuel costs climbed similarly. But exporters couldn't raise prices because of global competition from Ecuador, Vietnam, and Indonesia.

The result? Farmer margins dropped from 15-20% in 2022 to just 8-12% in 2026. The industry was in recovery mode, trying to stabilize operations and regain lost market share.

Then the Red Sea crisis hit.

The Current Disruption: Route Economics

Source: Shipping line schedules, port authority data, logistics industry reports

Source: Container shipping industry reports, Drewry Shipping Consultants, Freightos Baltic Index

Break down what actually changed and why it matters.

The Route Shift

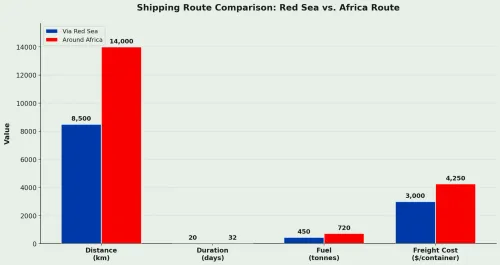

The old route via the Red Sea. A ship would leave from a Gujarat port, cross the Arabian Sea, go through the Red Sea and Suez Canal, pass through the Mediterranean, and reach a European port. The new route goes around Africa. The ship still starts from a Gujarat port and crosses the Arabian Sea. But instead of the Red Sea, it goes all the way around the Cape of Good Hope, then across the Atlantic Ocean to reach a European port.

Run the numbers on a standard 20-foot reefer container carrying 12 tonnes of frozen shrimp:

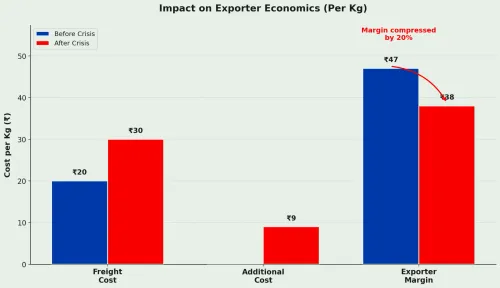

Old route cost per kg | ₹19-22 |

New route cost per kg | ₹28-32 |

Additional cost | ₹9-10 per kg |

Source: MPEDA, Visakhapatnam Port Authority

₹9-10 per kg doesn't look catastrophic on paper. But Exporters were working with ₹25-70 per kg margins. An additional ₹9-10 per kg freight cost is 15-35% of the margin.

Distance | ~8,500 km | ~14,000 km |

Duration | 18-20 days | 30-35 days |

Fuel Consumption | ~450 tonnes | ~720 tonnes |

Freight Cost (per 20-ft container) | $2,800-$3,200 | $4,000-$4,500 |

Source: Visakhapatnam Port Authority, shipping industry data

The Insurance Premium Spike

Marine insurance has jumped significantly too.

When ships used the Red Sea route, insurance was straightforward and relatively cheap. Now that vessels go around Africa, they're taking a much longer journey through waters with different risk profiles. Insurance companies have responded accordingly.

Marine insurance for a standard seafood shipment via the Red Sea route used to cost around 0.15-0.25% of cargo value. For a ₹10 crore shipment, that meant ₹1.5-2.5 lakh in insurance premium.

Now, with the African route, insurance has jumped to 0.40-0.60% of cargo value. For that same ₹10 crore shipment, the premium is now ₹4-6 lakh. That's a 150-200% increase in insurance costs.

Why insurance costs more:

The longer route means more time at sea, which means more exposure to weather risks, mechanical failures, and potential accidents. The African route also passes through areas with historically higher piracy risks, particularly around the Gulf of Guinea and parts of East Africa. Even though these waters are better patrolled now, insurers still factor in the risk.

Plus, reefer containers carrying frozen seafood have an additional risk layer. Any equipment failure during a 35-day voyage versus a 20-day voyage means higher chances of temperature variation and spoilage. Insurers price this in.

The combined hit:

For an exporter shipping 100 containers per month to Europe, the additional costs add up like this:

Freight increase: ₹9-10 per kg × 12 tonnes × 100 containers = ₹1.08-1.20 crore per month Insurance increase: ₹2.5 lakh per container × 100 = ₹2.5 crore annually or ₹20-21 lakh per month

Combined monthly impact: ₹1.28-1.41 crore in additional costs

Over a year, that's ₹15-17 crore in extra expenses just from freight and insurance, before accounting for any quality penalties or delayed payments.

But the 15-day extension in transit time creates problems beyond just higher costs. It raises a fundamental question for a perishable product: what happens to quality when your shipment spends 35 days at sea instead of 20?

The Shelf-Life Problem

Frozen shrimp has a technical shelf life of 18-24 months if stored at minus 18 degrees Celsius continuously. But there's a difference between what's technically safe and what buyers will pay premium prices for.

Long-term storage degradation:

Quality degrades over extended storage. In the first 0-3 months, shrimp maintains A+ quality grade, gets accepted by premium buyers, and commands 100% price. Between 3-6 months, it drops to A grade, gets bought by standard buyers, and fetches 95-100% of full price. At 6-9 months, quality becomes B+, appealing only to price-sensitive buyers who pay 85-95%. By 9-12 months, it's down to B grade, accepted only by discount buyers at 75-85% of original price.

The "fresh frozen" problem:

The real issue runs deeper. Most export contracts don't just specify quality grades. They specify "fresh frozen," which is a commercial classification, not a technical one. Fresh frozen means the product was frozen within 24 hours of harvest AND shipped within 30 days of freezing.

This is about market perception and buyer expectations, not actual spoilage. A shrimp that reaches the buyer in 45 days is technically still A+ grade by storage duration. But it's no longer "fresh frozen" by contract definition because it exceeded the 30-day shipping window.

Why buyers care:

Premium restaurants and supermarkets in the US and EU market their seafood as "fresh frozen" to consumers. When your shipment arrives on day 45 instead of day 25, it doesn't meet that classification. The buyer either applies a price penalty or reclassifies the product for a different market segment.

On a ₹10 crore shipment, that 5-10% penalty translates to ₹50 lakh to ₹1 crore in lost revenue. You're not being penalized for spoiled product. You're being penalized for breach of contract terms.

Contract Penalties

Most export contracts have specific clauses.

Delivery timeline clause:

The delivery window is plus or minus 5 days from the agreed date. For delays of 6-10 days, the penalty is 3-5% of invoice value. For delays of 11-15 days, it's 8-10% of invoice value. Beyond 15 days, the buyer can reject the shipment entirely.

Quality clause:

A temperature breach leads to immediate rejection. If the quality grade is below what was specified, there's a 10-15% price reduction. Shelf life concerns can trigger a 5-20% price reduction.

With 15-day delays becoming common, exporters are routinely paying 5-10% penalties.

The Inventory Pile-Up

When shipments get delayed, the domino effect starts:

Processing unit perspective:

A typical processing unit plans for weekly processing of 500 tonnes, weekly exports of 500 tonnes, and cold storage capacity of 2,000 tonnes, which gives them a 4-week buffer.

When shipping delays increase, the mismatch becomes obvious. Weekly processing continues at 500 tonnes because farms keep producing. But weekly exports drop to 350-400 tonnes because fewer ships are available. This means inventory builds up at 100-150 tonnes per week. After 8 weeks, you're looking at 800-1,200 tonnes of excess inventory.

The cost of holding:

Cold storage costs ₹3-5 per kg per month. Working capital gets locked up with interest running at 10-12% annually. And there's an opportunity cost because you can't process fresh batches.

For 1,000 tonnes held for 2 months, cold storage costs ₹60-100 lakh. Interest on working capital, assuming ₹600 crore value, adds another ₹50-60 lakh. Total holding cost comes to ₹110-160 lakh. This is a direct hit to cash flow.

The Compounding Cost Crisis

Put all these cost increases together to understand the full impact on an exporter's economics.

Take a mid-sized exporter shipping 100 containers per month to Europe. The costs have compounded:

Freight increase: ₹9-10 per kg additional cost. For 12 tonnes per container times 100 containers, that's ₹1.08-1.20 crore extra per month.

Insurance spike: Premium jumped 150-200%, adding ₹20-21 lakh per month.

Cold storage buildup: Excess inventory holding for 8 weeks costs ₹110-160 lakh.

Working capital lock: Extended payment cycle from 40 days to 58 days requires an additional ₹5 crore in working capital, costing ₹60 lakh annually in interest.

Contract penalties: 5-10% price cuts on delayed shipments further erode margins.

Total monthly impact: An additional ₹1.5-1.8 crore in costs, plus one-time working capital needs of ₹5 crore.

What this means for profitability:

Remember, exporters were already operating on margins of just 8-12% after the earlier cost pressures. Now add these new costs. For an exporter doing ₹10 crore in monthly business, an additional ₹1.5-1.8 crore in costs means margins have essentially been wiped out. Many are now operating at break-even or losses.

The viability question:

At what point does it stop making sense to export at all? When your margin drops from 10% to zero or negative, you're essentially working for free or losing money on every shipment. The rational response is to stop exporting until conditions improve.

The productivity spiral:

And this is exactly what's happening. Lower profitability is leading to lower productivity. Farmers are reducing harvest cycles from 3 per year to 2. Processing units are running at 60-65% capacity instead of 85%. Trawlers are making fewer trips. Each participant in the chain is pulling back because the economics don't work.

The result? Production itself is dropping by 10-15%. It's not just that exports are down because of shipping delays. Actual production is declining because participants are choosing not to produce when they can't make money.

First-Order Impact: The Direct Consequences

Quantify what's happening at each level.

Export Volumes Are Dropping

Data from MPEDA (Marine Products Export Development Authority):

The numbers month by month: In January 2026, normal exports would have been 85,000 tonnes, but actual exports were only 67,000 tonnes, a drop of 21%. February 2026 saw normal expectations of 90,000 tonnes, but only 69,000 tonnes actually shipped, down 23%. March 2026 was worse: against normal exports of 95,000 tonnes, only 72,000 tonnes moved, marking a 24% decline.

The drop is concentrated in Europe-bound shipments. US and Asia routes are less affected.

Why exporters are skipping shipments:

Does it even make sense to ship or not.

In Scenario 1, if you ship despite delays, the math looks brutal. Revenue is ₹700 per kg. Old freight was ₹22 per kg, but new freight is ₹32 per kg. You face a quality penalty of ₹35 per kg, which is 5%. Plus a delay penalty of ₹21 per kg, which is 3%.

Net realisation comes to ₹622 per kg. Cost of production is ₹580 per kg. Your margin? Just ₹42 per kg or 6.7%.

In Scenario 2, if you hold and wait, the numbers look different. Revenue could be ₹700 per kg if things improve. Freight would be back to ₹22 per kg if the Red Sea opens. No penalties.

Net realisation is ₹678 per kg. But your cost is ₹580 per kg plus ₹15 per kg for cold storage. Margin works out to ₹83 per kg or 12.3%.

But Scenario 2 has risk. What if the Red Sea doesn't open soon? What if quality degrades while waiting? Many exporters are choosing to reduce production rather than pick either option.

Price Realization is Falling

Even when shipments go through, buyers are negotiating prices down.

Typical negotiation:

Buyer: "Your shipment was 12 days late. Contract allows 10% penalty." Exporter: "Red Sea closure is force majeure." Buyer: "Fine, I'll take 5% off. But if you don't agree, I have Vietnam suppliers ready."

Result: Exporter accepts 5-7% price cut to maintain relationship.

Multiply this across thousands of transactions, and you get significant revenue loss.

Working Capital Lock-Up

This is crushing smaller exporters.

Normal working capital cycle:

The normal cycle runs like this. On Day 0, you harvest from the farm. By Day 2, processing is complete. On Day 5, the shipment leaves the port.

Day 25 sees the shipment reaching the buyer. And on Day 40, you receive payment. Total cycle: 40 days.

Current working capital cycle:

Now it's changed. Day 0 is still harvest time. Processing still completes by Day 2. But the shipment leaves only on Day 8 due to delayed scheduling.

The shipment reaches the buyer on Day 43 because of the longer route. And payment? That comes on Day 58 because the buyer delays it, citing late delivery. Total cycle: 58 days.

Impact on working capital:

An exporter doing ₹100 crore annual business needs different working capital now. Under the normal cycle, you needed ₹11 crore in working capital, which is 40 divided by 365, multiplied by 100. Under the extended cycle, you need ₹16 crore, which is 58 divided by 365, multiplied by 100. That's an additional requirement of ₹5 crore. At 12% interest, that's ₹60 lakh in additional annual cost.

Many exporters don't have access to this additional capital. They're forced to reduce operations.

Second-Order Impacts: The Ripple Effects

Now we get to the less obvious but equally important consequences.

Income Shock at Farm Level

When export demand drops, it immediately affects farm-gate prices.

Price transmission example:

The export price chain normally works. The FOB price (Free On Board, meaning the price when goods are loaded onto the ship), which is what the exporter gets, is ₹700 per kg. The price to the processor is ₹650 per kg, which accounts for the exporter's margin. And the price to the farmer is ₹550 per kg, which covers the processor's margin plus costs.

When exports slow and exporters cut back purchases, the pressure moves down the chain. The FOB price stays at ₹700 per kg because that's the unchanged international market price. The price to the processor remains at ₹650 per kg for the exporter's margin. But the price to the farmer drops to ₹480 per kg because the processor has excess inventory and reduces buying. The farmer's realisation drops by ₹70 per kg or 13%.

Impact on a typical farmer:

Take an average shrimp farm of 3 hectares. Production per cycle is 12 tonnes. Annual production is 24 tonnes across 2 cycles.

Old revenue was 24,000 kg multiplied by ₹550, which equals ₹1.32 crore. New revenue is 24,000 kg multiplied by ₹480, which equals ₹1.15 crore. The loss is ₹17 lakh per year.

After accounting for costs of ₹90 lakh, profit drops from ₹42 lakh to ₹25 lakh. That's a 40% hit. This affects around 60,000 shrimp farmers in coastal states.

Migration Pattern Disruption

This is subtle but real.

Over 2018-2023, coastal processing units created around 2.5 lakh jobs across several areas. These include processing and packaging, cold storage operations, quality control and grading, and logistics and transportation.

Many of these workers came from tier-2 and tier-3 cities. They were attracted by steady employment, salaries ranging from ₹15,000 to ₹25,000 per month, and accommodation provided by the units.

What's happening now:

Processing units running at 60-70% capacity are making changes. They're reducing shifts from 3 to 2 per day. They're cutting the temporary workforce. And they're reducing overtime opportunities.

Workers facing reduced income, dropping from ₹25,000 to ₹16,000, are now considering their options. Some are thinking about returning to cities for construction or service jobs. Others are looking at moving to other manufacturing sectors.

If 30% of the workforce migrates back, that's 75,000 workers. Coastal economies would lose ₹150 crore in annual wages.

Global Market Share Loss

This is the strategic damage.

How buyers think:

A US importer buying 500 tonnes per month of shrimp evaluates three things: reliability of supply, consistency of quality, and price competitiveness.

Indian exporters currently score 6 out of 10 for reliability, down from 9 out of 10 due to delays. Quality remains at 8 out of 10, unchanged. But price has dropped to 7 out of 10, down from 8 out of 10 due to freight costs.

Meanwhile, Ecuador scores 9 out of 10 for reliability because the Panama Canal route is unaffected. Quality is at 7 out of 10. And price is at 8 out of 10.

The switching cost:

Once a buyer develops a relationship with an alternative supplier, several things happen. New contracts are signed, typically for 12-24 months. Supply chains are reconfigured. Quality benchmarks are reset.

Winning back that buyer takes time and money. You need 6-12 months of consistent delivery. You need to offer price discounts of 5-10% initially. And you face additional marketing and relationship costs.

Look at India's market share in US shrimp imports. In 2024, it was 27%. In 2025, it dropped to 24% due to tariffs. For 2026, it's projected at 21% due to Red Sea issues combined with tariffs.

Ecuador's market share tells the opposite story. In 2024, they had 31%. In 2025, that grew to 34%. For 2026, it's projected at 37%.

Each 1% market share lost equals ₹600-700 crore in annual exports.

Supply Chain Imbalances

Multiple parts of the chain are getting misaligned.

Trawler operations:

Trawlers plan their fishing trips based on three factors: processing unit capacity, expected export orders, and fuel subsidy availability.

But there's another critical constraint: LPG shortage. Trawlers need LPG to cook meals and preserve catch during multi-day trips at sea. A typical 5-7 day fishing trip requires 3-4 LPG cylinders. With LPG supplies becoming erratic and subsidized quotas limited, many trawler operators can't secure enough cylinders to go out for extended trips. You can't ask a crew to spend 5 days at sea without cooking facilities or proper food storage.

When export orders drop 20-25% and LPG availability becomes uncertain, trawlers respond in several ways. They reduce trip frequency from 5 trips per month to 3-4 trips. They shorten trip durations, catching less per trip. And they start targeting domestic market species instead of export-oriented catches.

This creates underutilisation across the board. Boat capacity sits idle 30-40% of the time. Crew members earn less because of fewer trips. And maintenance facilities see lower utilisation.

Processing unit imbalance:

These units were built with certain assumptions. They planned for daily processing of 20 tonnes. Annual capacity was set at 6,000 tonnes. And they expected capacity utilisation at 85%.

Currently, they're running at lower levels. Daily processing has dropped to 13-14 tonnes. Annual capacity remains the same at 6,000 tonnes. But capacity utilisation has fallen to 60-65%.

The problem: fixed costs like rent, equipment depreciation, and permanent staff salaries stay the same. But revenue drops proportionally.

This is operating leverage in reverse — when fixed costs stay the same but revenue drops, margins compress faster than the revenue decline. At 85% utilisation, the margin was 15%. At 65% utilisation, the margin drops to just 6-7%.

Cold Storage Economics Under Stress

The cold storage sector is facing a peculiar problem.

Normal cold storage model:

A typical cold storage unit has a capacity of 5,000 tonnes. Normal occupancy runs at 70-75%, which means 3,500-3,750 tonnes. The rental model charges ₹4 per kg per month. Monthly revenue comes to ₹140-150 lakh. Operating cost is ₹95-100 lakh. Operating margin works out to ₹40-50 lakh.

Current situation:

Right now, occupancy has jumped to 95-100% because exporters are storing delayed shipments. Revenue looks good at ₹190-200 lakh.

The misreading:

The problem: some cold storage operators are seeing this high occupancy and making a critical error in judgment. They're reading temporary crisis-driven inventory backup as genuine demand growth. They see their units running at full capacity and think "business is booming, we need to expand."

But this inventory is only here because shipments are stuck, not because there's actual growth in the seafood business. Once the Red Sea route normalises, this backlog will clear within weeks. Occupancy will drop right back to the normal 70-75%.

Yet some operators are already investing in capacity expansion - building new cold storage units, adding warehouses - based on what they see today. They're essentially building infrastructure for a problem that will disappear. When the crisis resolves and occupancy returns to normal, they'll be stuck with expensive, underutilized facilities and debt from the expansion.

Domestic Price Distortion

This is where economics gets interesting.

Two opposite forces:

Force 1 suggests more supply domestically should make prices fall. Exports are down 20-25%. That volume stays in India. We're talking about an additional 1.5-2 lakh tonnes in the domestic market. This should push prices down.

Force 2 suggests reduced production should make prices rise. Farmers seeing low prices are reducing next cycle production. Trawlers are making fewer trips. Total production drops by 10-15%. This should push prices up.

What actually happens:

Different markets show different results.

In Andhra Pradesh, which is near production areas, shrimp prices are down 15-20%. The reason is excess supply from failed exports. Farmer stress is high.

In Odisha, the impact is particularly severe because the state has both inland and coastal fishing. Coastal shrimp farmers are facing the same export crisis as Andhra Pradesh - prices down 12-18%, inventory piling up, margins evaporating. But inland fisheries, which focus on freshwater fish for domestic consumption, are also suffering indirectly. Processing units that used to handle both marine and inland catch are now operating at reduced capacity, creating a bottleneck for inland fishermen too. The state is essentially getting hit on both fronts.

In Delhi and Mumbai, which are consumption centers, shrimp prices are down only 5-10%. The reason? Middlemen are absorbing some of the benefit. Consumer impact is minimal.

In Kerala, which has both production and consumption, fish prices are stable to slightly up. The reason is that export disruption mainly affects shrimp, not fish. Trawler economics are relatively better there.

This creates regional disparities in how the crisis affects different stakeholders.

Why Exporters Can't Just Sell Domestically

The obvious question: if export economics are broken, why not redirect the produce to Indian consumers?

Three structural reasons make this nearly impossible.

The domestic market for premium shrimp barely exists at scale. Export-grade vannamei shrimp (16-20 count, IQF processed) sells domestically at ₹340-450 per kg in retail markets — not dramatically lower than export realisations of ₹400-600 per kg. The price gap isn't the primary problem. The volume gap is.

India produces 1.78 million tonnes for export annually. The domestic premium shrimp market is a fraction of that — mostly concentrated in metros and coastal cities, mostly smaller grades, mostly fresh not frozen. One industry report notes bluntly: "The absence of a domestic shrimp market has been one of the key problems facing Indian producers as they rely heavily on international demand to support their prices." You can't dump hundreds of thousands of tonnes of export-grade frozen shrimp into a market that doesn't exist at that scale.

The business structure doesn't match. An international importer orders 100-200 tonnes per shipment, pays via Letter of Credit upfront, and works on 6-12 month contracts. A domestic restaurant chain orders 500 kg per month, pays on 30-60 day credit terms, and negotiates prices weekly. To replace one export relationship, you'd need contracts with 250-500 domestic buyers. The working capital, payment risk, and operational complexity are completely different businesses.

Cultural preferences are hyper-specific. Even in fish-eating regions, preferences are local. Kerala wants chemmeen (prawns) in curry or pickle form. Try selling that in Jammu & Kashmir where trout is traditional. Nagaland's fermented fish won't work in Punjab.

And even when Indians eat seafood, format matters. McDonald's has one fish burger. Burger King has zero seafood options. This isn't because Indians don't eat fish — Kerala, Goa, and West Bengal consume it daily. It's because Indians want fish in a thali, or prawn curry with rice, or grilled with masala — not a breaded patty in a burger bun. The same person who won't touch a fish burger will happily order a fish thali.

India's vannamei shrimp industry was built for export. The species was introduced in 2009 specifically to meet international buyer specifications. The processing infrastructure, quality certifications, cold chain logistics — everything is designed to get frozen shrimp from a coastal farm onto a container ship. Redirecting that to tier-2 Indian cities would require building an entirely different distribution network, for a product format domestic consumers don't want, targeting a market that doesn't exist at the volumes exporters produce.

The domestic market is large. But it's not a safety valve. It's a separate market entirely.

Government Response: What's Being Done

The government is attempting to provide relief through three main channels.

Export incentives: An additional 2-3% benefit under MEIS — the Merchandise Exports from India Scheme — for Red Sea-affected shipments (₹100-150 per kg) and a proposed freight subsidy covering 40-50% of incremental costs. Budget requirement: ₹500-700 crore. The challenge is preventing misuse while getting money to genuine exporters quickly.

Infrastructure push: Reducing port dwell time — the hours cargo sits waiting at the port — from (4-5 days to 2-3 days), faster customs clearance, and ₹2,700 crore for cold chain development. Problem: These are 18-24 month projects. The crisis needs immediate solutions.

Market diversification: Trade negotiations to increase exports to Middle East, Southeast Asia, Japan, and South Korea from 25% to 35-40% of total. Challenge: These markets already have established suppliers. Gaining share requires time and relationship building - this is a 2-3 year strategy, not a short-term fix.

None of these measures address the core issue: shipping routes. Until the Red Sea stabilizes or viable alternatives emerge, policy support can only soften the blow, not solve the problem.

Putting It All Together

India built a seafood export industry on four assumptions: stable shipping routes, predictable 20-25 day transit times, relatively stable freight costs, and just-in-time delivery — meaning shipments arrive exactly when buyers need them, with no warehousing delays. This worked for two decades. The Red Sea crisis broke it.

What makes this different from COVID or trade disputes is that it disrupts the fundamental logistics of a perishable, time-sensitive industry. You can't store shrimp for months waiting for routes to normalise. You can't ask buyers to wait 45 days instead of 25. You can't absorb 35% freight increases on 8-12% margins.

The cascading impact is clear. Freight and insurance costs spike, margins vanish, exporters stop shipping, farmers reduce production, and the entire supply chain contracts.

The fundamental question: Is this temporary or structural?

If the Red Sea normalises in 3-6 months, the industry can recover with losses contained around ₹1,500-2,000 crore. Market share losses to competitors would likely be temporary.

If disruption extends beyond a year, the risks multiply significantly. Market share could shift to Ecuador and Vietnam as buyers establish new supply relationships. Industry restructuring might become necessary. Losses could escalate to ₹5,000-7,000 crore. But the outcome isn't predetermined - aggressive market diversification, investment in alternative routes, and competitive pricing could help retain market position even in a prolonged crisis.

Government relief measures help but don't solve the core problem. Export incentives and infrastructure projects can't fix shipping routes. The industry is discovering that being globally integrated means being globally vulnerable, and there's no quick hedge for that.

Investor Takeaway

If you hold listed seafood exporters — Avanti Feeds (NSE: AVANTIFEED), Waterbase (NSE: WATERBASE), or Apex Frozen Foods (NSE: APEX) — you're carrying direct exposure to margin compression from the ₹9-10 per kg freight spike, quality penalties, and working capital stress described above. These companies derive 60-100% of revenue from exports and already operated on thin margins (8-12% EBITDA) before the crisis. The timeline matters: if Red Sea routes normalise by Q2 2027, losses stay contained at ₹1,500-2,000 crore and current weakness could present a 12-18 month buying opportunity. But if disruption extends beyond a year, market share shifts structurally to Ecuador and Vietnam, industry consolidation accelerates, and only large, well-capitalised players survive without significant dilution.

Watch three indicators: freight rates dropping below $3,500 per container, MPEDA export volumes returning to 90%+ of prior year levels, and management guidance indicating margin recovery. Until all three align, the risk-reward doesn't favour fresh deployment. For existing holders, Q1 FY27 and Q2 FY27 management commentary on working capital and export order pipelines will matter more than the quarterly numbers themselves.

Sources

- Marine Products Export Development Authority (MPEDA)

- Nielsen Retail Measurement Services

- Euromonitor International

- Visakhapatnam Port Authority

- Indian seafood industry reports and trade publications

- Blinkit and BigBasket product listings (for pricing data)

Data Sources for Charts and Tables

- Export volumes and values: Marine Products Export Development Authority (MPEDA) annual reports and monthly trade data

- Freight rate data: Container shipping industry reports, Drewry Shipping Consultants, Freightos Baltic Index

- Processing unit economics: Industry interviews and seafood processor association reports

- Cold storage capacity and pricing: Indian cold chain industry reports and trade publications

- Regional price data: Agricultural Produce Market Committee (APMC) market rates, wholesale market surveys

- Route analysis and transit times: Shipping line schedules, port authority data, logistics industry reports

- Company-specific data: NSE/BSE listed company annual reports and investor presentations (Avanti Feeds, Waterbase, Apex Frozen Foods)

The content in this blog is intended purely for educational purposes. Any securities or mutual funds referenced are illustrative in nature and do not constitute a recommendation or endorsement by Kotak Neo. Investors are encouraged to assess their own financial situation and seek professional advice before making any investment decisions. For compliance T&C and disclaimers, Visit https://www.kotakneo.com/disclaimer/

0 people liked this article.