India's Concert Economy: The Multi-Sector Play Investors Are Missing

- 15 min read

- 1,008

- Published 04 May 2026

How a generation's hunger for experiences became one of the most significant economic shifts of the decade

It was the dying moments of a concert at Lollapalooza 2026. The lights were still blazing. The last notes from the string section had settled. The crowd was screaming. Yungblud's frontman Dominic Harrison broke into tears. In a post-concert interview, he said: "I promise to come here every year till I am dead. The love I have received is crazy." This is not a scene from LA, New York, or Shanghai. It is from the Mahalakshmi Racecourse in Mumbai.

Easy to read that scene as a feel-good cultural moment. But there is a harder, more interesting story underneath. That concert did not happen just because a young musician loved his Indian fans. It happened because India had become a market -- a serious, scalable, economically meaningful market for live entertainment. And the numbers that have built up around it in the last few years tell the story of an industry that is not merely growing. It is transforming.

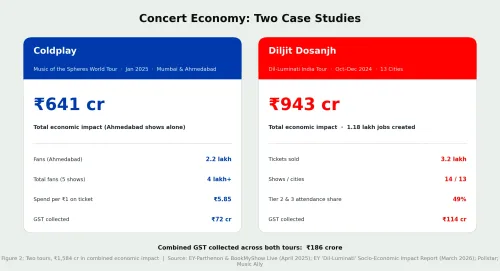

And if you want to understand what that growth looks like in the real world, two concerts tell the story better than any chart.

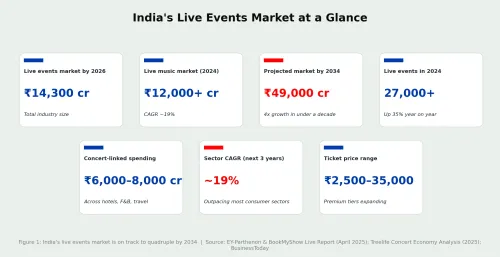

That ₹5.85 multiplier is the number worth sitting with. For every rupee someone spent on a Coldplay ticket, they spent nearly six more rupees on hotels, flights, restaurants, and shopping. A concert is not just a concert. It is a demand trigger for an entire spending ecosystem -- one that hotels, airlines, food chains, and apparel brands all benefit from. And as India's live events market grows from ₹14,300 crore today to a projected ₹49,000 crore by 2034, that multiplier effect compounds across the whole economy.

So how did we get here? And why does it matter to you as an investor?

The 2010s: When India Started Performing Its Life Online

The 2010s were an important decade. Companies were expanding aggressively into India and China. Better jobs followed. Businesses thrived. Disposable incomes rose. And that rising income needed somewhere to go.

At the same time, the social media wave hit. Everyone was on Facebook, posting pictures and updates about their trips, birthdays, and daily lives. Whether you had bought a new car or taken a break to the nearest hills -- it was out on social media for the world to like and comment on. Everyone became a minor celebrity.

Then came short videos. You were no longer just capturing a smile or a mountain -- you could capture how you felt in that place. TikTok started that obsession globally in 2016, but after it was banned in India in 2020, Moj, Josh, and Instagram Reels stepped straight into that gap. Indian audiences did not miss a beat.

Here is the economic consequence of that shift. Once people started documenting and sharing their lives online, the things worth sharing changed. An expensive watch sits in a drawer. A concert, a food festival -- these generate content. They are inherently shareable. And in a world where your social identity is built on what you share, the purchase that gives you something to post becomes more valuable than the purchase that sits silently on a shelf.

This was not just a lifestyle preference. It was a fundamental reallocation of consumer spending. Social media was the slow-burning fuse -- quietly redirecting rupees from products to experiences, one reel at a time.

How Covid Ruined Everything -- and Then Made Everything Better

Then Covid arrived. And it did not accelerate this trend -- it detonated it. The outdoors became out of reach for most Indians. We were cooped up in our homes, and even a walk around the block became difficult.

The lockdown created claustrophobia, suffocation, and loneliness. After a point, e-commerce players were allowed to deliver clothes, bags, and gadgets to our doorsteps. We had our things, but we no longer had our moments -- under the sun, quite literally.

This is the critical distinction for understanding what happened next. Social media had been slowly shifting preferences for a decade. But Covid did something more fundamental -- it stress-tested the value of every category of spending by making one category completely unavailable.

When you cannot go out, cannot gather, cannot share physical space with other human beings, you understand very quickly which purchases were filling a deep human need and which ones were just habit. Things sat in your wardrobe. Experiences were what you missed. That lesson was not forgotten when the lockdowns ended.

So when the pandemic ended, young people took to the outdoors with a vengeance. The self-worth metric had shifted completely -- from "I own things" to "I do things." Young people, with higher disposable incomes and a fresh memory of what it felt like to have nothing to do, wanted to belong to a larger collective and share an emotion.

Sports and concerts gave them that collective feeling. Rooting for your favourite team or artist made you feel part of a tribe. Concerts over a designer handbag. Sports tickets over expensive sneakers. Gen Z was reconstructing the value pyramid -- and for investors paying attention, that reconstruction was rerouting crores of rupees away from traditional consumer goods and into experiences, hospitality, food, entertainment, and travel.

How Event Management Companies Changed to Meet the New Needs

Media and event management companies read this shift early and moved fast. They reorganised themselves -- from event managers to experience creators, effectively reinventing their core. And with that reinvention came a new commercial logic: better experiences command higher ticket prices, attract bigger sponsors, and generate more ancillary spending. The economics of live events had fundamentally improved.

Ticket prices are now decided using data: city-wise demand, price sensitivity, and fan behaviour. Apps like District and BookMyShow push real-time notifications so the right audience always knows what is coming -- and the conversion from awareness to purchase has never been faster or more direct. That purchase flow is itself a business: BookMyShow processes crores of transactions and earns on every one.

The technology transformation cannot be overlooked either. From generic speakers to international-grade sound systems like D&B Audiotechnik and L-Acoustics. From static lighting to synchronised light shows with large LED screens, visuals, and animations.

Coldplay's concerts in Ahmedabad and Mumbai used imported LED rigs, real-time crowd monitoring through 400+ CCTV systems, and accessibility features including sensory rooms. Zoned entry, RFID and QR-based ticket scanning, and better crowd-flow management have eased the concerns of global artists and given audiences a sharply better experience. Better experiences drive more demand. More demand drives higher prices. Higher prices attract bigger artists. It is a flywheel -- and it is spinning.

Why Artists Decided to Come to India

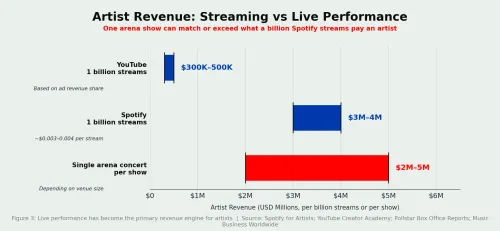

Sure, fans wanted to see Katy Perry and Dua Lipa perform at a large stadium. But what was in it for the artist? The answer lies in how the music industry's revenue model was quietly dismantled and rebuilt over the last 25 years.

In the early part of this century, artists earned royalties -- a percentage of what record labels made from selling music. Streaming platforms changed that model fundamentally. Today, a billion streams might pay an artist a few hundred thousand dollars -- a fraction of what a single world tour stop generates.

Live performance became the primary revenue engine. And for global artists watching their streaming listener counts, Indian fans had become too significant to ignore. Indians were not just playing their music. They were influencing popularity rankings, keeping songs on algorithm-driven playlists, and generating the kind of engagement data that labels and talent managers track closely. Touring India was no longer a goodwill gesture. It was a financially rational decision backed by data.

What the Future Looks Like

The experience economy does not stop at concerts. It is bleeding into every format where a young, connected, economically active audience can gather and share. Two examples show where the frontier is moving.

The first is bhajan clubbing. Picture a room full of young people -- sitting cross-legged on mats, incense in the air, soft mandala projections dancing on the walls -- while a live band plays a high-energy fusion of devotional bhajans and modern electronic beats. No alcohol. No chaos. Just collective chanting, swaying, and what attendees describe as a "clean high."

What started as intimate Mumbai living-room gatherings around 2021 has grown into stadium-scale events drawing up to 15,000 attendees by late 2025. Radhika Das's kirtan concerts drew 8,000 people to Delhi's Yashobhoomi Convention Centre. These are ticketed events with sponsors, merchandise, and brand partnerships. Prime Minister Modi referenced bhajan clubbing during Mann Ki Baat.

The commercial point is this: a new event format that did not exist five years ago is now filling arenas, attracting sponsors, and generating ticket, merchandise, and brand revenue. That is new money entering the experience economy -- not replacing existing events, but expanding the market.

The experience economy is here to stay. It keeps evolving with the changing tastes of the Indian audience -- and every new format it spawns is a new revenue stream, a new category of sponsors, and a new reason for people to travel, stay in hotels, eat out, and dress up.

What It Means for You: The Indian Investor

The experience economy is not a niche trend confined to concerts or ticketing platforms. It is a spending shift — and like most consumption shifts in India, it cascades across sectors. What begins as a ₹5,000 concert ticket rarely ends there. It expands into flights, hotel stays, food, merchandise, and digital transactions. For investors, the opportunity lies not at the point of origin, but across this entire value chain.

Media, Ticketing, and Content: The Core Layer

The most direct monetisation layer remains ticketing and content ownership. BookMyShow's parent, Bigtree Entertainment, dominates ticketing infrastructure but remains unlisted — forcing public market investors to look for proxies rather than pure plays.

Among listed names, PVR Inox is repositioning itself from a cinema exhibitor to a broader out-of-home entertainment platform, increasingly experimenting with live events and alternative content formats. Saregama represents a more interesting structural play. As streaming consumption rises alongside concert buzz, the value of its music catalogue (IP) compounds. Its role as a co-promoter in the Diljit Dosanjh Dil-Luminati tour signals a shift: music companies are no longer passive royalty earners, but active participants in live monetisation ecosystems.

Hospitality: Demand Spikes Become Earnings Events

Large-format concerts are now city-level economic events, not just entertainment events. The Coldplay concerts in Ahmedabad (January 2025) offer a clear data point: ~1.38 lakh travellers, ~980 additional flights, and fully booked trains. For a non-traditional tourist city, this translates directly into sharp spikes in hotel occupancy, higher average room rates, and short-duration but high-intensity revenue bursts.

Companies like Lemon Tree Hotels and Chalet Hotels, with exposure to mid-market segments and non-metro locations, are structurally positioned to benefit as more events move beyond Tier 1 cities.

Aviation: Filling the Gaps in Demand

Concert-driven travel introduces a different kind of passenger: leisure-driven, event-specific, time-bound. This demand is particularly valuable because it fills non-business travel windows, improves load factors on weekend and off-peak routes, and expands traffic to Tier 2 destinations. Airlines like InterGlobe Aviation (IndiGo) and SpiceJet benefit not from ticket pricing power alone, but from better capacity utilisation — a key driver of profitability in aviation.

Food & Beverage: Immediate Consumption Capture

Of the estimated ₹6,000–₹8,000 crore annual concert-linked spending, a significant share flows into food and beverage consumption — both inside venues and in surrounding areas. This makes QSR and food chains one of the most direct and immediate beneficiaries of the experience economy. Listed players such as Devyani International (KFC, Pizza Hut), Jubilant FoodWorks (Domino's), and Westlife Foodworld (McDonald's India) stand to benefit from high footfall density and impulse consumption during event cycles.

Apparel: A Behavioral Shift in Discretionary Spend

A more subtle but emerging trend is the rise of event-linked fashion consumption, particularly among Gen Z. Concerts and festivals are increasingly "occasion-based dressing moments", driving incremental demand for fast fashion, ethnic fusion wear, and statement outfits. Companies like ABFRL, Vedant Fashions, and Trent are positioned to capture this shift, although this remains an early-stage, sentiment-driven tailwind rather than a fully visible earnings driver.

Payments & Fintech: The Invisible Infrastructure Layer

Every experience economy transaction — from ticket purchases to in-venue spending — flows through digital payment rails. The rise of RFID wristbands, cashless venues, and high-frequency micro-transactions increases transaction volumes and engagement for payment platforms. Players like One97 Communications (Paytm) and the broader fintech ecosystem benefit from scale and frequency, even though they remain one step removed from the core experience.

Real Estate & Infrastructure: Building for Scale

As event frequency and scale rise, so does the need for dedicated physical infrastructure: large arenas, amphitheatres, and multi-use stadiums. This creates a long-term opportunity in commercial real estate and venue development. Companies such as DLF, Brigade Enterprises, and Nesco are potential beneficiaries as the ecosystem moves from temporary setups to permanent infrastructure.

Advertising: Budgets Follow Engagement

Brands are increasingly reallocating budgets toward experiential marketing, driven by digital ad fatigue and higher engagement in physical events. The Diljit Dosanjh tour, with 15+ brand sponsors (including Air India, HDFC, Levi's, Coca-Cola), illustrates how concerts are becoming multi-brand marketing platforms. This signals a broader shift where events evolve into advertising inventory, not just entertainment products.

Festivals: The Underpriced Opportunity

Traditional cultural festivals like Durga Puja and the Hornbill Festival are beginning to undergo professionalisation: structured ticketing, curated travel packages, brand partnerships, and international marketing. As these formats mature, they can transition from cultural gatherings to scalable economic events. The beneficiaries will likely include hospitality chains near festival hubs, travel and booking platforms, and media companies owning cultural IP. This segment remains under-analysed and underpriced, making it one of the more interesting long-term themes.

The Investor Takeaway

This is not a single-sector opportunity — it is a consumption-layer shift with multi-sector spillover effects. The smartest way to approach it is to identify immediate beneficiaries (F&B, hospitality), scalable monetisation layers (media, IP), and long-term enablers (infrastructure, payments).

The real insight is simple but powerful: The value is not created where the experience begins — it is created where the spending spreads. India has 1.4 billion people. For decades, the world staged its best shows somewhere else, and Indians watched on YouTube the next morning. That era is over. India is now on the setlist — and it is not just a stopover.

Sources

-

EY-Parthenon & BookMyShow Live -- "India's Rising Concert Economy: Coldplay's Ahmedabad Tour Sets the Blueprint for India's Next Cultural Boomtowns" (April 2025)

-

EY India -- "Dil-Luminati India Tour 2024 -- Socio-Economic Impact Report" (March 2026)

-

Pollstar Box Office Reports -- Coldplay Music of the Spheres World Tour, India shows (January 2025)

-

BusinessToday -- "India, Go Live! The $1.72 Billion Cue for Economy from Coldplay's Ahmedabad Concerts" (January 2025)

-

Treelife -- "A Snapshot of the Concert Economy: Insights from Coldplay" (2025) Music Ally -- "Diljit Dosanjh's Dil-Luminati 2024 India Tour Had an Economic Impact of $103M, Says EY" (March 2026)

-

MSEED (Bhavans College) -- "The Sacred Rave: Mapping the Rise of Bhajan Clubbing in India" (2026)

-

India Today -- "Bhajan Clubbing Goes Big, and It's Selling Out Like a Concert" (November 2025)

-

Billboard / Box Office Mojo -- Wicked worldwide box office gross data (2025) BookMyShow platform data; District app data; industry estimates

This article is for informational purposes only and does not constitute financial advice. It is not produced by the desk of the Kotak Securities Research Team, nor is it a report published by the Kotak Securities Research Team. The information presented is compiled from several secondary sources available on the internet and may change over time. Investors should conduct their own research and consult with financial professionals before making any investment decisions. Read the full disclaimer here.

Investments in securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed SEBI prescribed limit. The securities are quoted as an example and not as a recommendation. SEBI Registration No-INZ000200137 Member Id NSE-08081; BSE-673; MSE-1024, MCX-56285, NCDEX-1262.

0 people liked this article.