DMart’s 500th Store: The Machine Nobody Can Copy

- 15 min read

- 1,130

- Published 22 May 2026

On March 31, 2026, DMart opened 12 stores in a single day. Daund. Tiruvottiyur. Avadi. Zundal. Eight other towns. That pushed the total count to 500, and the stock jumped nearly 9% the following morning — its biggest single-day move in over a year.

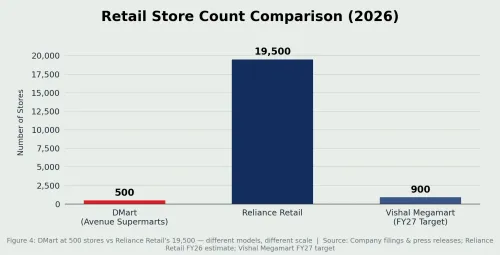

Five hundred stores sounds like a big number. Against Reliance Retail’s 19,500, it’s almost modest. But the number of stores was never really the point. The more interesting story is what those 500 stores represent — how a retail company quietly became the first choice for cost-conscious India’s monthly essentials run, and why no one else has been able to build the same thing in 24 years.

Let’s start with a timeline, because the shape of DMart’s growth tells you something the numbers alone don’t.

Two things jump out. First, how long DMart stayed small by choice — 29 stores after eight full years, while Big Bazaar already had 250. Second, how sudden the acceleration is. From a slow, deliberate crawl to 85 stores in a single financial year, with Big Bazaar long gone by the time the sprint began.

That slowness was not a stumble. It was a choice. DMart spent two decades perfecting a machine. Now it is confident enough to run it faster.

So what is the machine?

The business model

Walk into a DMart store and the first thing you notice is what isn’t there.

No mood lighting. No music playing overhead. No elaborate displays or celebrity-endorsed brands arranged at eye level. The store looks, in many ways, like a slightly larger neighbourhood no frills supermarket store in an Indian metro. Shelves stacked with dals, rice, cooking oil, storage containers, cleaning supplies. Utility goods. Daily essentials. Nothing more.

That absence is the business model.

DMart runs no loyalty programmes. It has no celebrity ambassadors, no IPL sponsorship, no social media campaigns engineered to go viral. It rarely announces discounts or runs limited-period offers. Instead, it does something far harder to sustain: it keeps prices low every single day. The tagline — Every Day Low Prices, Every Day Low Cost — is not a marketing line. It is an operating philosophy. The store doesn’t need a campaign because the price on the shelf is the campaign.

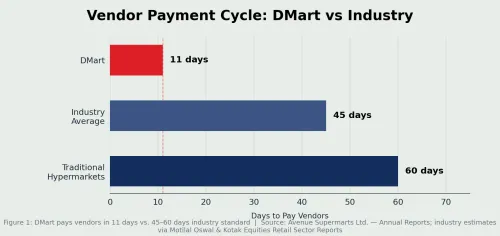

The first pillar of that philosophy is how DMart manages its suppliers. It comes down to one number: 11 days. That is how long DMart takes to pay its vendors. The industry standard is anywhere between 30 and 60 days.

To understand why this matters, think about what life looks like for a mid-sized FMCG — fast-moving consumer goods — manufacturer in India. You produce goods, you ship them to a retailer, and then you wait. Six weeks, typically. All while you still need to buy raw materials, pay factory workers, and fund the next production cycle. You are, in effect, giving the retailer an interest-free loan whether you want to or not. Now imagine a buyer walks in and offers to pay you in 11 days. Every time. Without exception. That was DMart. And vendors responded the only rational way they could — they offered better prices.

Over time, this also creates something beyond price leverage — it creates priority. When there is a supply crunch, DMart gets served first. When a vendor launches a new product, DMart gets early access. These advantages compound quietly over years in ways that no contract can manufacture.

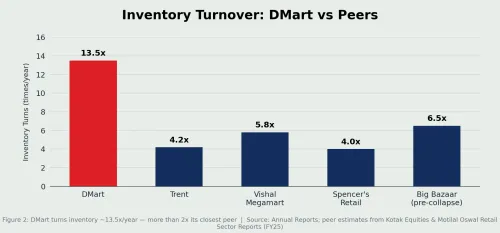

The mathematics are straightforward. Being paid in 11 days instead of 45 days is worth roughly 2 to 3 percent of the invoice value to a vendor, given normal borrowing costs in India. That 2 to 3 percent is what DMart captures as a lower purchase price — and passes directly to the customer as a lower shelf price. This is not a discount strategy. It is a financial structure. DMart is essentially pre-financing the vendor’s working capital and being compensated through cheaper procurement. The byproduct of this is a business that generates enough internal cash to fund its own growth — a customer walks in, pays at the till immediately, and the vendor gets paid on day 11. Its inventory turns roughly 13 to 14 times a year, which means the business is cycling through its stock — and collecting cash — continuously. Debt is a tool, not a flaw — and plenty of successful businesses use it well. What is specific to DMart is that its model generates enough cash internally that borrowing was never a necessity. That distinction matters most when conditions turn — a business that grows on its own cash flow has no interest payments to service when revenues slow.

Big Bazaar was once what DMart is today — the go-to for cost-conscious India’s daily essentials. That story ended in bankruptcy. The reasons are worth a piece of their own.

The second pillar is real estate. Most retailers rent their stores. This keeps capital light in the short run but creates a permanent liability — monthly lease obligations that don’t pause when sales slow, and landlords who can renegotiate terms when a location turns valuable. DMart does the opposite. It buys the land and builds the store. No rent escalations. No eviction risk. No landlord with leverage.

Every DMart store is an asset on the balance sheet, not a liability. As property values have risen across Indian cities and Tier 2 towns, the real estate DMart acquired years ago has only become more valuable. The company built a retail business and ended up with a substantial property portfolio as a byproduct.

The third is returns — or rather, the near absence of them. DMart’s product mix of staples, daily essentials, and groceries has a near-zero return rate. Nobody sends back a bag of rice. And DMart has leaned into this deliberately. On its online platform DMart Ready, apparel purchases carry no return or exchange policy — a stance that has frustrated some customers but is entirely consistent with the model. The business was never designed around discretionary purchases. It was designed around products where the customer already knows what they want before they walk in. That clarity eliminates an entire layer of reverse logistics cost that most retailers quietly absorb.

The bigger you get, the cheaper you become

There is one more dimension to the vendor relationship that compounds in DMart’s favour as it scales.

Most businesses raise prices when they can and cut them reluctantly when forced to. DMart’s prices fall automatically as it grows — not because of competitive pressure, but because of how the machine works. Every new store DMart opens increases its total purchase volume across all vendors. Higher volume means better procurement prices — not as a one-time negotiation, but as a permanent re-pricing of the relationship.

Those savings pass directly to the customer as lower shelf prices. The 500th store doesn’t just generate its own revenue. It makes every one of the preceding 499 stores marginally more competitive on price.

This creates an asymmetry that new entrants find very difficult to bridge. A competitor opening its first 50 stores cannot match DMart’s procurement prices because DMart is buying for 500 stores. By the time that competitor reaches 200 stores, DMart is at 700. The gap does not close — it widens.

And when any retailer runs a sale, the lower price ends when the promotion does. When DMart’s prices fall, it is because the business got more efficient. The lower price is permanent.

Why nobody has copied it

The model looks simple on paper. Pay vendors fast. Own your stores. Keep prices low. Stock only what moves quickly. Yet in 24 years, no Indian retailer has successfully replicated it.

The reason is that every element of the model depends on every other element. You can only pay vendors in 11 days if your cash conversion is fast enough. Your cash conversion is only fast enough if inventory turns are high. Inventory turns are only high if you stock a limited, disciplined range of fast-moving products. And you can only maintain that discipline if you are willing to say no — to thousands of product lines that don’t move fast, to manufacturers who want shelf space in exchange for fees, to the temptation of stocking higher-margin but slower-moving items.

That kind of refusal requires patience. Most retail businesses don’t sustain it. Reliance Retail has the capital to theoretically compete, but its model — built around roughly 19,000 smaller-format stores serving different shopping occasions — is not something it can simply pivot away from. The DMart model is the accumulated result of 24 years of compounding decisions. You cannot buy that with a cheque.

DMart’s model is clear. The more contested question is whether anything can disrupt it.

Quick Commerce Isn’t Taking DMart’s Customers

For the past two years, the dominant narrative in retail analysis has been that quick commerce — the 10 to 20 minute delivery services like Blinkit, Zepto, and Swiggy Instamart — poses an existential threat to DMart. The stock has faced pressure on this thesis. Analysts have written cautionary notes. Management has been asked about it on every earnings call.

The narrative rests on a category error.

1. Different shopping missions, not the same customer

DMart’s core customer is a price-conscious family doing their monthly stock-up — 10 kilograms of rice, five kilograms of dal, cooking oil, cleaning supplies, storage containers. The Blinkit customer is someone ordering a small pack of biscuits at 11 at night. These are not the same basket, or the same moment. The overlap is thinner than it appears. India’s consuming class is vast and varied — and for the majority of it, a Rs 30 delivery fee on a Rs 200 order is not an afterthought. It is a reason to plan ahead and go to DMart instead.

2. Segmentation, not substitution

What is actually happening across Indian households is segmentation, not substitution. The same family does both. Monthly essentials from DMart, because the savings on a large basket are real and meaningful to a household budget. Snacks for a late-night gathering from Blinkit, because speed matters and the basket is small enough that the price premium doesn’t register.

DMart and quick commerce have divided the shopping occasion between them, not the customer.

3. Speed has a cost — and DMart isn’t paying it

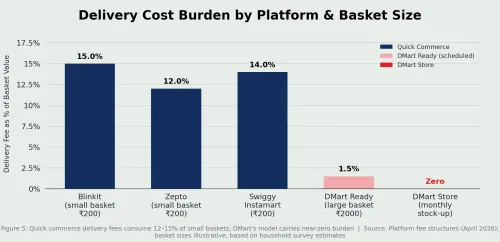

DMart does offer home delivery through DMart Ready, but the deliveries are scheduled rather than instant. A customer places an order and picks a delivery slot — typically choosing from windows available over the next few days, not the next few hours. There is no promise of 20 minutes or even same-day delivery in most cases.

The slots are usually offered in 2-3 hour windows — say, 8 AM to 10 AM, or 3 PM to 5 PM — and customers book them at least a day in advance, sometimes more depending on demand in their area. This might look like a limitation compared to the instant gratification promised by quick commerce platforms. It is actually a deliberate cost control mechanism.

Scheduled deliveries allow DMart to batch orders going to the same neighbourhood, optimise delivery routes based on known demand patterns, and run fulfilment operations at a fraction of the cost of on-demand delivery. Instead of keeping riders idle waiting for orders to come in, DMart can plan logistics around confirmed slots. Instead of maintaining expensive dark stores in high-rent locations, DMart fulfils from its regular retail stores where the inventory is already sitting. The trade-off is clear: customers sacrifice speed and convenience for price. And for monthly grocery runs where the basket is large and planning is expected, that trade-off makes economic sense.

Blinkit and Swiggy Instamart are built around speed — dark stores, idle riders, and the infrastructure to fulfil an order in minutes. That speed has a price, and right now the platforms are absorbing it.

DMart never signed up for that race.

4. The economics of quick commerce are still not proven

Both Blinkit and Swiggy Instamart are still loss-making. Customers are not paying the true cost of a 20-minute delivery — the platforms are subsidising convenience to build habit and scale. The day the economics have to stand on their own, the price gap between a quick commerce basket of staples and the equivalent at DMart becomes very difficult to justify for a budget-conscious household.

What about the other challengers?

Quick commerce is not the only competitive narrative around DMart. Trent — the Tata Group retailer behind Zudio and Westside — and Vishal Megamart are both growing fast and increasingly showing up in the same conversations. But proximity in conversation is not the same thing as overlap in business.

1. Different stores, different jobs

Trent is a fashion-led business. Zudio is where a young professional buys an affordable kurta for a wedding. Westside is where a family shops for occasion wear. Star supermarkets add a grocery layer, but the brand identity is not built around staples — it is built around apparel. Vishal Megamart is a broad-format hypermarket: a family in a Tier 2 town browses toys, curtains, and clothing on a Sunday afternoon. DMart is where that same family buys its rice, dal, and cooking oil every month.

These are not competing for the same basket. DMart’s core — non-negotiable daily essentials — is the category where price sensitivity is highest and switching costs are lowest. Essentials are not aspirational. They are habitual. And habit, once anchored to price, is hard to break.

A shopper might experiment with where they buy a shirt. They rarely experiment with where they buy their atta.

Where competition actually shows up

The consumer lens above applies cleanly in urban and semi-urban markets. But in Tier 2 cities, the picture is more complicated. This is where basket compositions blur, where the hypermarket and the grocery run start to overlap, and where DMart and Vishal Megamart are genuinely competing for the same footfall.

2. Two expansion philosophies, one battleground

Vishal Megamart is moving fast — targeting around 900 stores by FY27 with smaller formats designed specifically for smaller towns. The strategy is volume and velocity: get in early, get in cheap, establish the habit before the competition arrives.

DMart is moving differently. Its own outgoing CEO acknowledged the company should have had 600 to 650 stores by now — an unusually candid admission that the pace has been conservative even by DMart’s own standards. The 85-store push in FY26 is, in part, an attempt to close that gap. But the approach remains the same: own the land, control the economics, do not compromise on the discipline.

This is not just an operational difference. It is a philosophical one. Vishal is betting on speed. DMart is betting on structure.

This is one of the few places where DMart is genuinely being tested — not on category, but on conviction.

What this means for the Indian retail investor

For someone considering DMart as part of their portfolio, the structural question is not whether the 500-store milestone is impressive. It is whether the business that produced it can keep compounding at the same rate — and whether the current price already reflects that.

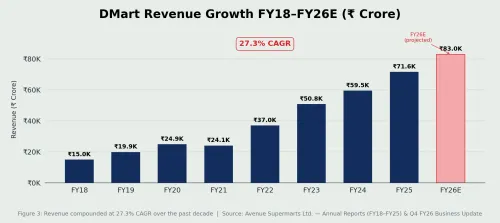

The numbers give some context. DMart’s trailing twelve-month revenue stands at Rs 64,226 crore, with Q4 FY26 alone clocking Rs 17,204 crore — up nearly 19% year-on-year. Over the past decade, the company has compounded sales at a median rate of 27.3% a year. The market cap sits at roughly Rs 2,38,000 crore, with a price-to-earnings ratio of around 88. By conventional metrics, that is an expensive stock. What the market is pricing in is the continuation of the machine.

Whether that confidence is priced correctly is a judgement call every investor has to make for themselves. But the underlying business logic — faster payments, lower procurement costs, lower shelf prices, higher volumes, repeat — has not broken down in 24 years, including through demonetisation, GST implementation, a global pandemic, and the rise of e-commerce.

The risk worth watching is not quick commerce, for the reasons already discussed. The more meaningful risk is execution — specifically, whether the rapid expansion into Tier 2 cities introduces the kind of operational complexity that erodes the discipline the model depends on. Opening 85 stores in a single year is a different challenge from opening 29 stores in eight years. The machine has more moving parts now. Whether the culture of saying no travels as cleanly to Daund and Avadi as it did in Mumbai is the question the next three to five years will answer.

For a retail investor with a long time horizon, DMart is one of the cleaner examples in the Indian market of a business with a structural — not cyclical — edge. The machine is real. The question, as always, is the price you pay to own a piece of it.

Where this is going

The 500-store milestone is not a reaction to competition. It is an expansion into territory that competition cannot easily follow — Tier 2 cities where quick commerce will not operate profitably for years, where the price-sensitive, bulk-buying household is the dominant consumer type, and where DMart’s model compounds most cleanly.

And the machine that got DMart here — paying vendors in 11 days, owning its stores, stocking only what moves, saying no more than it says yes — is not getting weaker as it scales. It is getting stronger.

That is the actual story behind the number.

Sources

- Avenue Supermarts Limited — Annual Reports (FY18–FY25) — store count data, revenue growth, inventory turns, vendor payment cycle, real estate ownership model

- Avenue Supermarts Limited — Q4 FY26 Business Update & Quarterly Business Updates — Q4 FY26 revenue (Rs 17,204 crore), FY26 store openings (85 stores), 500-store milestone (March 31, 2026), trailing twelve-month revenue (Rs 64,226 crore)

- Avenue Supermarts Limited — FY17 Annual Report — outgoing CEO comments on store expansion pace (600–650 store target)

- National Stock Exchange (NSE) — DMart (Avenue Supermarts) share price data — 9% single-day stock move, market capitalisation (~Rs 2,38,000 crore), price-to-earnings ratio (~88)

- Kotak Equities — Retail Sector Reports — peer estimates, inventory turns comparison, industry payment cycle benchmarks

- Motilal Oswal — Retail Sector Research (FY25) — vendor payment cycle industry estimates, peer comparisons

- Reliance Retail — Company filings & press releases (FY26) — Reliance Retail store count (~19,500)

- Vishal Megamart — Company filings & press releases — FY27 store target (~900 stores), smaller-format expansion strategy

- Trent Limited (Tata Group) — Annual Reports — Zudio and Westside brand positioning

- Zomato Limited — Blinkit segment disclosures — loss-making status, dark store model

- Swiggy Limited — Swiggy Instamart segment disclosures — loss-making status, on-demand delivery model

- Platform fee structures & household survey estimates (April 2026) — delivery fee as percentage of basket value

- Future Group — Public filings and press coverage — Big Bazaar collapse (2021), store count history

- DMART Ready — Platform terms and conditions (April 2026) — scheduled delivery model, no-return apparel policy

The content in this blog is intended purely for educational purposes. Any securities or mutual funds referenced are illustrative in nature and do not constitute a recommendation or endorsement by Kotak Neo. Investors are encouraged to assess their own financial situation and seek professional advice before making any investment decisions. For compliance T&C and disclaimers, Visit https://www.kotakneo.com/disclaimer/

0 people liked this article.