China’s Economic Wall is Cracking, And the Tremors are Reaching Your Portfolio

- 15 min read

- 1,076

- Published 17 Apr 2026

Six crore apartments. Just let that number sink in for a moment. That is the number of housing units sitting empty across China right now: built, finished, unsold and slowly gathering dust. To put that in perspective, that is more than twice the total number of homes in India's four largest cities combined.

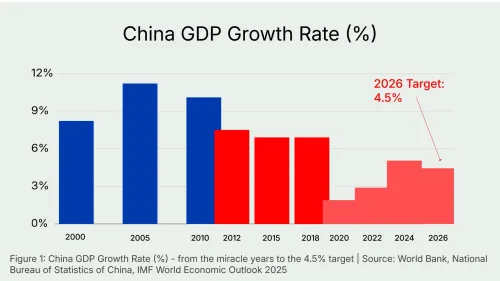

China set its 2026 growth target at 4.5% earlier this month, its least ambitious goal since 1991. And that headline number only tells part of the story. The country also slipped into deflation for two consecutive years: a phenomenon not seen since the Asian Financial Crisis of 1998, and one that is fundamentally at odds with an economy that officially claims to be growing at 5%.

But to understand why any of this matters to you as an Indian investor, we need to go back to where it all began.

The Miracle That Was

Since 1978, China did something no country had ever done at that scale: it grew at double digits for over three decades. It did this by doing one thing exceptionally well: making things cheaply and selling them to the world, while building the infrastructure to keep doing so at an almost incomprehensible scale, along with providing tax incentives and industry-favourable regulations to all who wanted to set up shop in China.

34 ports. 259 airports. Over 5,500 railway stations. 2,000 special economic zones. That is the total number today.

By 2010, China had overtaken Japan to become the world’s second-largest economy with a nominal GDP of $6.1 trillion. Made in China goods were flooding markets across the global south (India included).

But by 2012, the engine had started to sputter. Wages had risen. Vietnam, India and Mexico were undercutting China on labour costs. The post-2008 world was buying less. The country that had grown at 10% for thirty years was now looking at 7–8%. And rather than accept that slower growth was the new normal, China doubled down: banks kept lending, factories kept producing, steel kept getting made, not because there was demand for it, but because stopping the machine was politically unthinkable. The result was a catastrophic overcapacity problem across nearly every sector.

To absorb all that excess capital and keep the GDP numbers healthy, China made a massive push on one sector above all others: real estate.

Figure 1: China GDP Growth Rate (%) — from the miracle years to the 4.5% target | Source: World Bank, National Bureau of Statistics of China, IMF World Economic Outlook 2025

The Real Estate Unravelling

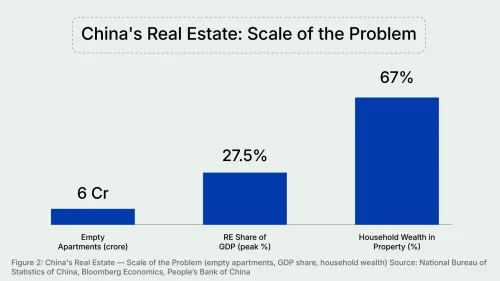

At its peak, property and construction accounted for nearly 25–30% of the entire Chinese economy. Developers borrowed aggressively. Local governments became addicted to land sale revenues. And ordinary Chinese citizens poured their life savings into apartments, not to live in, but as investments. Two-thirds of household wealth in China was now sitting in property. The trap was set.

Figure 2: China's Real Estate — Scale of the Problem (empty apartments, GDP share, household wealth) | Source: National Bureau of Statistics of China, Bloomberg Economics, People’s Bank of China

What followed was not a crash in the traditional sense. It was something slower and, in many ways, more damaging: a prolonged, grinding collapse that is still unfolding.

Construction starts in China in 2024 had halved compared to 2019 levels. New home prices across major cities have been falling for two consecutive years. Developer after developer began missing debt payments, cancelling projects and leaving homebuyers with paperwork for apartments that may never be finished.

The crisis spread quickly beyond the usual suspects. Country Garden, the largest private property developer in China as recently as 2022, warned of losses in the range of 45 to 55 billion yuan (roughly ₹52,000 crore to ₹63,000 crore) in just the first half of 2023. Vanke, once considered one of the more conservative and stable developers, put land up for sale at a 29% discount just to service its debts and saw its sales fall 43% year over year. In January 2025, Chinese authorities detained Vanke’s CEO and began planning a government-led reorganisation of the company.

Evergrande: The Goliath That Fell

Evergrande was born in 1996, right as China's urbanisation boom was taking off. It grew fast, borrowed faster, and by 2018 was ranked the world's most valuable real estate brand. Its founder, Xu Jiayin, was briefly China's wealthiest man.

The model was simple and, for a long time, extremely lucrative: borrow heavily, build quickly, sell fast, use that cash to borrow more and build again. When Evergrande could sell 500 billion yuan (roughly ₹5.8 lakh crore) worth of property in a year, it had enough cash flow to stay ahead of its debts.

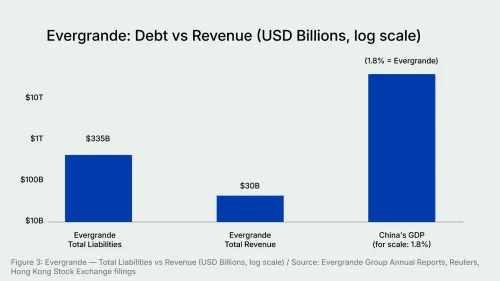

Then Beijing blinked. Alarmed by the reckless leverage spreading across the property sector, the government introduced the “three red lines” policy in 2021: a set of strict debt limits that developers had to meet or face restrictions on new borrowing. For Evergrande, which had built its entire existence on an endless cycle of debt, this was a death sentence. By 2022, Evergrande’s total liabilities exceeded $335 billion (roughly ₹28 lakh crore), more than ten times its total revenue and roughly 1.8% of China’s entire GDP that year.

Figure 3: Evergrande — Total Liabilities vs Revenue (USD Billions, log scale) | Source: Evergrande Group Annual Reports, Reuters, Hong Kong Stock Exchange filings

In December 2021, Evergrande officially defaulted on its debts, triggering shockwaves in the Chinese and Hong Kong stock markets. Its founder was eventually detained. In January 2024, a Hong Kong court ordered the company to liquidate. Its shares, which once traded at HK$31, had fallen 99% to less than two cents before trading was suspended. In August 2025, Evergrande was formally delisted from the Hong Kong Stock Exchange. It was the final chapter of one of the most spectacular corporate collapses in history.

The deeper damage was not to Evergrande’s shareholders. It was to the psychology of the Chinese consumer. When your apartment, which represents two-thirds of your family’s wealth, is losing value, you stop spending. You stop buying the new phone, taking the holiday, upgrading the car.

No Jobs, No Spending: Inside China’s Consumption Freeze

China’s internal consumption story has quietly become as worrying as the real estate story. Youth unemployment hit 18.8% in 2024 among those aged 16–24. But that number deserves scrutiny before you take it at face value. When the rate hit a record 21.3% in June 2023, Beijing did not fix the problem. It stopped publishing the data. When reporting resumed six months later, the methodology had been quietly revised to exclude students, part-time workers, and those not actively looking for work. Many analysts believe the true figure is significantly higher.

For context, the OECD average for youth unemployment is around 10.5%. India’s youth unemployment, for all its challenges, sits well below China’s current official rate. A record 12.22 million university graduates entered the job market in 2025, up 430,000 from the previous year, into an economy battered by a trade war with the US and structural disruption from AI. More than 20% of drivers for China’s two largest food delivery platforms now hold college degrees. At least 70,000 hold master’s degrees. This is what graduate employment looks like in China today.

That last number deserves a closer look because it seems to contradict something we will say shortly about China’s ageing population. How can you have a record graduating class and an ageing population at the same time? The answer lies in a demographic echo. The enormous cohorts born in the 1980s and 1990s, just before China’s One Child Policy fully took hold, are still producing graduates today. Think of it like a river: the water flowing out now was fed by heavy rains decades ago. The rains have long stopped, but the river is still full. Birth rates in China have been collapsing since the mid-2000s. In 2023, China recorded more deaths than births for the second consecutive year, something that had not happened since the famine of the early 1960s. The 12.22 million graduates of 2025 are in all likelihood a high watermark. The graduating classes of the 2030s will be dramatically smaller. So China is caught in a peculiar bind: too many young people looking for jobs right now, and not enough young people to sustain the economy a decade from now. India, for comparison, is on the opposite end of this curve. India’s median age is around 28. China’s is already 40 and climbing. This divergence is one of the most significant long-term structural differences between the two economies.

The result is a generation that is spending less, saving more and, in some cases, opting out of the conventional milestones of adult life altogether. The Chinese internet has a term for it: “lying flat” (躸平, tǎng píng), the opposite of the hustle culture India’s own urban youth grew up with. And when the world’s most populous country decides to check out of the economic race, the ripples reach everywhere. Savings pile up in banks instead of flowing into the economy. Shops sit quieter than they should. And with domestic consumption refusing to fire, there is no engine inside the country ready to pick up the slack.

What It Means For You: The Indian Investor

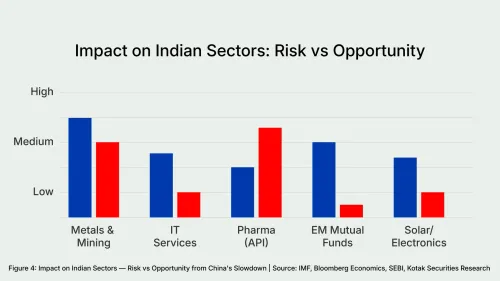

For Indian investors, the link is this: when Chinese consumers stop spending, global brands, commodity producers and technology companies that depend on Chinese demand all feel it. And when those companies feel it, they tighten budgets, defer projects, and shrink the pool of work flowing to Indian IT services and manufacturing exporters. The consumption freeze in China is not just China’s problem. It is already showing up in sectors and asset classes that many Indian retail investors hold directly or indirectly.

Figure 4: Impact on Indian Sectors — Risk vs Opportunity from China's Slowdown | Source: IMF, Bloomberg Economics, SEBI, Kotak Securities Research

The Metals Play

China is the world’s largest consumer of steel, copper and aluminium. When Chinese construction activity slows, commodity demand falls, and prices come under pressure globally. Global steel consumption fell 0.2% in 2024 and is expected to decline another 1% in 2025, with China’s real estate slowdown as the primary driver. For Indian investors, this means stocks like Tata Steel, JSW Steel, Hindalco and Vedanta face real pressure from suppressed global commodity prices, even as India’s own infrastructure spending remains strong. The Nifty Metal index is particularly sensitive to Chinese demand signals, and any further deterioration in China’s construction data will likely weigh on it.

There is, however, a flip side. India is now the world's second-largest steel producer, and as global manufacturers diversify away from China, India's metals sector could benefit from supply chain reorientation over the medium term.

The Pharma Angle

India exports a significant portion of its Active Pharmaceutical Ingredients (APIs) to China. A slowdown in Chinese domestic consumption and healthcare spending could soften demand for Indian APIs. At the same time, as Western pharma companies look to reduce their dependence on Chinese API suppliers, Indian pharma companies are well positioned to absorb that business, a risk and an opportunity sitting in the same sector, depending on how events unfold.

IT Services: The Sector Facing Pressure from Two Directions

Indian IT is already navigating one of the most significant structural disruptions in its history. AI models that can write, review and debug code are fundamentally challenging a business model built on billing for human hours of development work. That is why Nifty IT has been under sustained pressure, and that pressure has nothing to do with China and everything to do with the economics of software services being quietly upended by AI.

China’s slowdown adds a second, separate layer on top of this. When global growth softens (and a stumbling Chinese economy is a key contributor), enterprise technology budgets at American and European companies get cut. CIOs defer discretionary projects, slow digital transformation spends and renegotiate contracts, shrinking the total pool of work available to TCS, Infosys and Wipro. Indian IT is the one sector in this story facing simultaneous pressure from two entirely different directions: one structural, one cyclical. Neither is going away any time soon.

Your Mutual Funds

If you hold international or emerging market funds, check whether they have China exposure. Many EM funds have significant allocations in Chinese equities, which have been volatile in the last few years. Domestically, the indirect pressure on metals and commodities sectors means thematic metal funds or sectoral funds with heavy commodity weightage deserve a closer look at their China sensitivity.

The Currency and Import Angle

A weakening yuan makes Chinese exports cheaper globally, including in India. This is already visible in solar panels, electronics and consumer goods, where Chinese competition is intensifying. For Indian companies in these sectors, a prolonged yuan depreciation is a competitive threat worth watching.

The bottom line for the Indian retail investor: China’s slowdown is not a catastrophe for Indian markets. In fact, the supply chain diversification story is a genuine opportunity for Indian manufacturing. But it is a live risk in your metals holdings, your EM fund allocations and any sector exposed to global commodity prices. Knowing where your portfolio touches China is the first step to managing it.

What Does the Future Look Like for China?

There are no easy fixes here. The IMF projects China’s growth will slide to around 3.3% by 2029 as demographic challenges, weak productivity and a structurally impaired property sector take their toll. The population is ageing rapidly. The working-age population is shrinking. And the government’s traditional lever of infrastructure spending is running into the wall of already-high local government debt.

But here is what the doom narrative misses: China is not going to collapse. The country that built 34 ports and 2,000 special economic zones in a generation does not simply fold.

By 2024, China’s state-led investment in its semiconductor industry alone exceeded $150 billion (about ₹12.5 lakh crore), roughly three times the funding earmarked under America’s own CHIPS Act. DeepSeek, which stunned the global AI community earlier this year with a model that matched Western capabilities at a fraction of the cost, was built in China, under chip sanctions. In 2024, China’s exports of ships grew 57%, semiconductors 17%, and electric vehicles 15%: a clear signal that the country is successfully climbing the value chain even as its old growth engines sputter.

China also dominates the mining of rare earth metals, extracting between 60–70% of the world’s supply, resources that every electric vehicle, smartphone and fighter jet on the planet depends on. Beijing is not standing still on the domestic front either: it has rolled out stimulus, cut interest rates and tried to shore up developer financing.

The story of China over the next decade is not one of collapse. It is one of a painful, slow, structural transition from an economy built on concrete and debt to one built on chips and clean energy. That transition will be messy, uneven and deflationary for the world. And that is precisely why it matters to you.

Sources

- IMF World Economic Outlook, 2024 and 2025 projections

- Bloomberg Economics — China GDP and property sector estimates

- ING Think — China trade surplus data, January 2025

- South China Morning Post — China trade surplus and export breakdown, January 2025

- Council on Foreign Relations — China export growth analysis, 2024

- Reuters — Evergrande default and liquidation reporting

- National Bureau of Statistics of China — Youth unemployment data

- The Diplomat — China semiconductor and AI infrastructure analysis, September 2025

- General Administration of Customs, People's Republic of China — Trade data 2024

The content in this blog is intended purely for educational purposes. Any securities or mutual funds referenced are illustrative in nature and do not constitute a recommendation or endorsement by Kotak Neo. Investors are encouraged to assess their own financial situation and seek professional advice before making any investment decisions. For compliance T&C and disclaimers, Visit https://www.kotakneo.com/disclaimer/

0 people liked this article.