The Auto Boom That Dealers Don’t Quite Trust

- 6 min read

- 7,757

- Published 22 May 2026

There was a time when buying a car in India felt like a family event.

Neighbours gathered, coconuts broken, garlands hung over side mirrors, and the first drive was less about speed and more about pride.

Owning a vehicle meant arrival.

Today, the showrooms are brighter, the loans easier, and the numbers far bigger.

India just clocked 2.97 crore vehicle sales in FY26, the highest ever.

On paper, it looks like the same celebration, just at scale.

But if you stand a little longer in those showrooms, past the balloons and the sales boards, you start noticing something else.

The smiles feel measured.

The conversations linger a bit longer on discounts, on inventory, on what might come next.

Because while the headline says boom, the dealer seems to be reading a footnote.

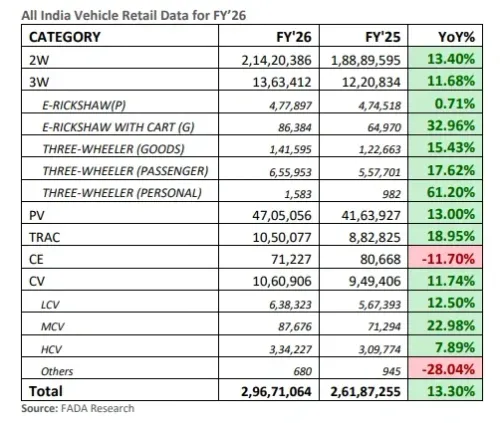

The Year That Looked Perfect

Source: FADA Research

Start with the numbers, because they are hard to ignore.

Two-wheelers crossed 2.14 crore units, up 13.4%.

Passenger vehicles touched 47.05 lakh units, growing 13%.

Commercial vehicles rose 11.7%, tractors surged 18.9%, and even three-wheelers held steady with double-digit growth.

It is one of those rare years where almost every segment showed up to the party.

Almost.

Construction equipment quietly slipped by 11.7%.

It is not the kind of number that makes headlines, but it is the kind that makes investors pause.

Because construction equipment does not follow consumption, it leads it.

When it slows, it usually whispers something about projects being delayed, capex being reconsidered, or momentum cooling before it shows up elsewhere.

And that is where the story starts bending.

Two Engines, One Slowing Slightly

Auto demand in India has always run on two engines.

The first is affordability.

When policies align, taxes ease, and financing becomes smoother, demand picks up almost instantly.

GST tweaks did exactly that not too long ago, giving the sector a visible push.

The second is fuel economics.

It is quieter, but far more persistent.

Every buyer calculates the running cost before committing.

Fuel prices do not just affect usage.

They shape the decision to buy in the first place.

Right now, the first engine has already done its job.

The GST tailwind has been absorbed into the system.

What remains is the second engine, and that is where discomfort is building.

Surveys suggest 36.5% of the dealers are already reconsidering purchase decisions because of rising fuel costs.

Not stopped, not reversed, just slowed.

And in markets like autos, slowing is often the first sign before something more visible.

The Inventory That Refuses to Leave

There is another quiet detail sitting in the background, and it has nothing to do with demand at first glance: inventory.

The ideal level for dealerships is about 21 days.

It keeps things efficient, liquid, and manageable.

What they have been dealing with instead is closer to 40 days, even after festive corrections.

As recently as mid-2024, it was even worse, touching 60+ days.

Now, inventory is one of those things that does not show up in headlines.

But it sits on balance sheets, quietly accumulating cost.

Financing costs rise, storage costs creep in, and discounting becomes less of a strategy and more of a necessity.

Which explains why dealers are selling more, but not necessarily earning more.

Margins That Refuse to Cooperate

The strange part about this cycle is that volumes look strong, but profitability does not follow as neatly.

Dealer margins in auto retail are typically in single digits.

The real money often comes from financing deals, insurance, and after-sales services.

But even those are under pressure.

Interest costs on inventory are rising.

Staffing and training expenses are going up.

Digital investments are no longer optional.

EV infrastructure needs upfront capital without immediate returns.

So, while the top line expands, the bottom line feels tighter.

It is running faster on a treadmill that is slowly tilting upward.

The EV Shift That Complicates the Picture

Then comes the transition that everyone agrees is inevitable, but no one finds easy in the short term: electric vehicles.

The numbers are already meaningful.

Three-wheelers have a 60.95% EV share, two-wheelers are at 6.54%, and passenger vehicles are at 4.25%.

But the speed of that shift is exactly what keeps dealers uneasy

Technology changes quickly, which means inventory risks increase.

What sits in the showroom today may feel outdated sooner than expected.

There are added costs in training teams, setting up charging, or servicing infrastructure, and selling a product the customer hasn't fully decided to trust yet.

Then there is resale value.

Still uncertain, still developing.

And uncertainty is rarely a friend of smooth retail cycles.

Supply Chains That Refuse to Stay Quiet

As if demand-side signals were not enough, supply has its own mood swings.

About 53% of dealers are already reporting supply or dispatch disruptions, linked to global tensions.

When components travel across continents, even a small disruption somewhere far away shows up as delayed deliveries or mismatched inventory here.

Popular models become scarce; slow-moving ones pile up.

A Rural Cushion, An Urban Pause

All India Vehicle Retail Strength YoY comparison for FY’26

Source: FADA Research

There is also a geographical nuance that is easy to miss.

Two-wheelers are increasingly rural-driven, with about 56% contribution from rural markets in early 2026.

That provides a cushion, a kind of steady base that keeps volumes moving.

Urban markets, especially for passenger vehicles, are facing more visible affordability pressure.

Higher costs, tighter financing conditions, and fuel sensitivity make the urban buyer more cautious.

Which is why the growth looks broad-based, but the quality of that growth varies.

What Dealers Are Really Saying

When over 50% of dealers expect only moderate growth going into April, it does not negate the record year that just passed.

It simply reframes what comes next.

Dealers are not reacting to what has happened.

They are responding to what they see forming.

And right now, what they see is a mix of absorbed tailwinds and building headwinds.

Reading This as an Investor

For investors, this is where the narrative shifts from celebration to interpretation.

FY26 numbers for companies like Maruti, M&M, and Tata Motors will look strong, as they should.

The demand was real, and the volumes came through.

But markets do not price the past.

They lean into what might change.

If fuel prices remain elevated, the most sensitive segment is the entry-level urban buyer, which makes companies like Maruti more exposed to that shift.

M&M, with its stronger rural SUV and tractor exposure, sits in a relatively more resilient pocket of demand.

Also, remember that quiet 11.7% dip in construction equipment?

That may be the earliest signal of where broader capex sentiment is drifting.

Ancillary players like Samvardhana Motherson Group carry an additional layer of global supply chain risk, which becomes relevant in a volatile environment.

Bajaj Auto, with its export exposure and rural demand linkages, finds itself in a slightly different equation altogether.

The Quiet Gap Between Data and Mood

Something is fascinating about this moment.

On one side, you have a record 2.97 crore vehicles, growth across segments, and a sector that looks alive and well.

On the other side, you have the dealer watching inventory, tracking fuel prices, worrying about supply, and adjusting expectations.

Both are true.

And markets, more often than not, move when that gap between what is reported and what is felt starts to widen.

The interesting question isn't whether FY27 will match FY26.

It's whether the dealer's footnote will become next year's headline.

Sources and References:

- MONEYCONTROL

- FADA

- AUTOCARPRO

- ECONOMICTIMES

- REUTERS

- LINKEDIN

- LIVEMINT

- SAHI

- FINANCIALEXPRESS

- DCFMODELING

The content in this blog is intended purely for educational purposes. Any securities or mutual funds referenced are illustrative in nature and do not constitute a recommendation or endorsement by Kotak Neo. Investors are encouraged to assess their own financial situation and seek professional advice before making any investment decisions. For compliance T&C and disclaimers, Visit https://www.kotakneo.com/disclaimer/

0 people liked this article.