When Tax Stability Becomes the Real Policy Choice

- 4 min read

- 1,005

- Published 30 Jan 2026

The quietness in this Budget season feels deliberate, almost studied.

No loud promises.

No last-minute slab theatrics.

Just a steady hum in the background.

Like a market that knows it does not need to shout to be heard.

If you have been around long enough, you learn that when policy stops trying to impress, it usually has something more serious on its mind.

To understand why, it helps to pause on the sheer scale of the tax machinery today.

Gross tax revenue for 2025–26 is estimated at ₹42.70 lakh crore, with net tax revenue at ₹28.37 lakh crore.

These are not numbers you casually tinker with.

GST alone sits at ₹11.78 lakh crore in the Budget Estimates, corporate tax at ₹10.82 lakh crore, and income tax collections at ₹14.38 lakh crore.

At this altitude, even a half-percentage point tweak stops being a reform and starts becoming a balance-sheet event.

When Big Numbers Change the Tone

Early tax collection data hints at where the nervousness comes from.

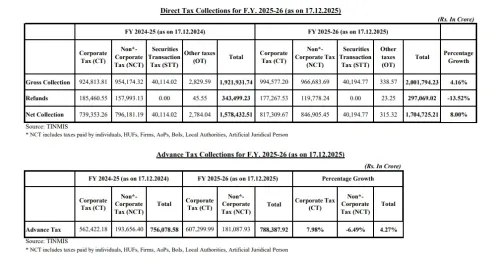

Net direct tax collections as of 17 December 2025 are at about ₹17.05 lakh crore, up roughly 8% year-on-year.

Respectable, but not exuberant. Scratch beneath that, and refunds start telling their own story.

Gross corporate tax collections are around ₹9.25 lakh crore.

But refunds of about ₹1.85 lakh crore sit alongside them.

The net picture is far less clean than headlines suggest.

GST behaves in much the same way.

Gross GST collections till 31 December 2025 stand at about ₹16.50 lakh crore, up 8.6%, while net GST is closer to ₹14.25 lakh crore, growing at 6.8%.

December itself throws up an interesting contradiction.

Net domestic GST revenue fell 5.1% month-on-month, even as GST from imports surged.

Demand is there, yes, but it is not purely homegrown.

Imports are doing more of the heavy lifting than many would like to admit.

Source: Ministry of Finance

Why Nobody Is Promising You a Tax Cut

This is where the expert commentary starts sounding eerily aligned.

SBI Research expects the Centre’s fiscal deficit to hover around 4.2% of GDP in FY27 and warns that any slowdown in nominal GDP growth will squeeze tax revenues further.

CareEdge goes a step further and flags a potential shortfall of up to ₹3 lakh crore in gross tax collections for FY26.

These are not alarmist forecasts.

They are arithmetic, and markets respect arithmetic more than optimism.

Against this backdrop, the idea of sweeping income tax cuts starts to look less like generosity and more like recklessness.

Multiple analysts have already pointed out that fiscal headroom is limited.

Any meaningful tax relief would either require sharp spending cuts or a willingness to let deficits drift.

Neither sits comfortably when capital is cautious and global conditions remain uneven.

Stability as a Design Choice

What is interesting is that this restraint is not accidental.

Predictability seems to be the policy now.

The new Income-tax Act, 2025, was designed to simplify and stabilise, not to be endlessly reworked.

Earlier Budgets did have their moments of generosity, including a one-off rebate structure that effectively exempted incomes up to ₹12.75 lakh.

That chapter, for now, appears closed.

What follows is incrementalism, not reinvention.

There is a practical reason for this caution.

When tax receipts are this large, a permanent rate cut creates a permanent hole.

A 0.5 percentage-point change can wipe out tens of thousands of crores.

Markets understand that such gaps do not vanish.

They reappear later as borrowing, inflation, or surprise levies.

Stability, even if boring, keeps those ghosts away.

Why Markets Like Boring Budgets

There is also the matter of cash flow timing.

Direct tax refunds already run into large numbers, as the ₹1.85 lakh crore corporate refund figure shows.

Sudden policy shifts complicate administration.

They also push more money out of the system upfront.

Add GST into the mix, and Centre–state equations come into play.

States are budgeted to receive over ₹14.22 lakh crore as their share of Union taxes in 2025–26 .

Any aggressive GST tinkering changes not just revenue totals, but federal dynamics. Layer this onto the macro backdrop.

The RBI is expected to keep the policy repo rate steady at around 5.25%.

Inflation is moderate, but the rupee has flirted with record lows, and capital flows remain fickle.

In such an environment, fiscal credibility does more for asset prices than a flashy tax announcement ever could.

Investors price stability faster than they price generosity.

Reading the Signal Beneath the Noise

This is where the second-order effect kicks in.

When tax rules stop changing every year, long-term capital breathes easier.

Valuations stretch a little more comfortably.

Risk-taking becomes selective rather than speculative.

Short-term traders may miss the fireworks, but longer-term investors quietly gain something better: visibility.

The message, if you listen closely, is not about lower taxes.

It is about few shocks and fewer surprises.

A tax system that behaves like an anchor rather than a lever.

For markets, that is not a disappointment; it is a signal.

In a world addicted to headline cuts and instant gratification, a boring Budget can be reassuring.

Predictability is not the absence of policy.

It is policy choosing not to shock capital.

And for anyone trading or investing with a longer memory, that might be the most valuable cue of all.

Sources and References:

- DEA

- PIB

- TIMESOFINDIA

- DDNEWS

- ECONOMICTIMES

- INCOMETAXINDIA

- TAXGURU

- BUSINESSTODAY

- THEHINDUBUSINESSLINE

- INCOMETAXINDIA

- CNBCTV18

- REUTERS

0 people liked this article.