India’s 2026 Growth Is Assembled, Not Organic

- 5 min read

- 4,947

- Published 23 Jan 2026

Big numbers have a way of commanding attention.

They arrive neatly packaged, confident, and reassuring.

The kind that make headlines feel settled before the questions even begin.

But spend enough time watching economies and you start trusting instincts more than percentages.

You learn to pause when growth looks a little too tidy.

To listen not just to how fast something is moving, but how much support it seems to need underneath.

It is a bit like watching a machine running smoothly.

No noise. No visible strain.

Yet someone is constantly feeding it fuel, tightening bolts, keeping the belts from slipping.

Speed alone does not tell you whether the system is comfortable or being held together.

India’s growth story today feels similar.

Strong on the surface. Carefully stabilised.

Powered as much by support structures as by momentum.

It increasingly feels like India’s growth story is less a wild forest and more a carefully arranged garden.

Beautiful, productive, and assembled leaf by leaf.

But the way it is being built is what matters the most.

Cities That Look Busy But Feel Tired

Walk through the data on urban India, and the shine dulls a little.

The urban worker population ratio sits at 46.8% as of June 2025.

It sounds precise, but feels tight when you imagine how many people are still waiting to be absorbed into formal jobs.

Wages have been doing an even quieter act.

Inflation-adjusted pay growth for listed companies stayed below 2% for three quarters of 2024, which is another way of saying salaries showed up to work but forgot to grow.

Banks, once reliable urban employers, are shifting their stance.

Private banks trimmed staff in FY25 while PSU and small finance banks added selectively.

The bigger pause comes from IT, the great urban wage engine.

Across the Big Five IT firms, net hiring over the past 9 months was just 17 people.

A hiring freeze dressed up as business discipline.

Yes, urban per capita spending still towers at ₹6,996 compared to ₹4,122 in rural India for 2023–24, but real growth in urban spending has slowed enough to narrow that gap.

Cities are spending, but not with the carefree confidence of rising incomes.

That distinction quietly matters.

Fragile urban demand changes which kinds of businesses feel dependable.

Rural Calm That Comes With A Catch

Rural India tells a more nuanced story.

According to NABARD, 42.2% of rural households saw income growth, while 15.7% reported a decline.

The share of households under stress is the lowest since FY06, which sounds like relief, and to some extent, it is.

Inflation perceptions softened to around 3.8%, and rural capital investment has helped steady nerves.

But then there are crop prices.

Bengal gram trading between ₹4,260 and ₹5,813 per quintal against an MSP of ₹5,875 is not a rounding error.

That is a loss of ₹800 to ₹1,200 per quintal for farmers.

Procurement delays and registration problems are the villains here, quietly undoing the good work elsewhere.

Rural incomes are breathing, but they are not singing.

Consumption survives, not because prices are rewarding effort, but because something else is stepping in.

Credit as the Co-Star: Spending Without Wage Support

That something else is leverage.

Banks posted 14.5% year-on-year loan growth in December, with retail and SME lending doing the heavy lifting.

Fintech lending has been even more enthusiastic.

Between September 2024 and September 2025, fintech loan books grew 36.1%.

Consumption kept moving, even as risks in unsecured lending quietly built up in the background.

Credit card outstanding growth slowed to 7.7% by October 2025, but household leverage remains elevated.

Nominal pay hikes of 9 to 10% look decent on paper.

Inflation quietly eats away at that comfort.

As a result, real wages remain stagnant for many segments of the workforce.

And what we have come to know is that credit-driven spending can come about quickly, but it also fades away just as fast.

The State Steps In: Transfers as a Substitute for Income

The real stabiliser of this story wears a policy badge.

Direct Benefit Transfers crossed 210.5 crore transactions in FY26, with cumulative payouts touching ₹43.95 lakh crore by May 2025.

That is cash flowing directly into households, supporting spending even when incomes hesitate.

The Union Budget doubled down.

Food subsidy allocations stood at about ₹2,03,420 crore, MGNREGA at ₹86,000 crore, and PM-KISAN at roughly ₹63,500 crore for 2025–26.

Together, they form a safety net sturdy enough to hold up consumption.

This is not organic income growth.

It works, but it works differently.

This is a demand being held in place with careful hands.

Consumption Without a Flywheel

By September 2025, private consumption had climbed to 62.5% of nominal GDP.

It is impressive, but also revealing.

When spending becomes the backbone of growth without incomes rising underneath, the economy becomes sensitive to any wobble.

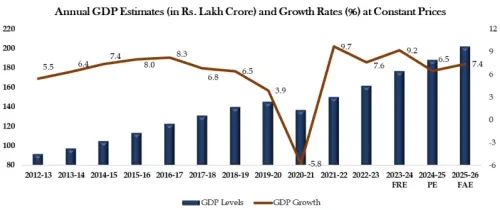

Q2 FY26 real GDP growth clocked in at 8.2% year-on-year, helped by fiscal pushes and investment bursts that feel distinctly one-off.

The International Monetary Fund nudged India’s FY26 growth forecast to 7.3%, then calmly pencilled in a slowdown to 6.4% for FY27.

Even typically optimistic global institutions are hinting that this pace may not linger. GST collections tell a similar tale.

December 2025 brought in ₹1.745 lakh crore, buoyed by strong consumption.

Credit grew at around 15% year-on-year, while deposits lagged, pushing credit to deposit ratios higher.

Demand is rising because credit is available, not because savings are swelling.

Retail deal volumes recovered to $3.4 billion in Q3 2025, but activity clustered around textiles and e-commerce.

Narrow recoveries make for selective opportunities, not blanket optimism.

This is growth that moves because it is supported by credit, transfers and policy and not because incomes are pulling it forward on their own.

Source: Government of India

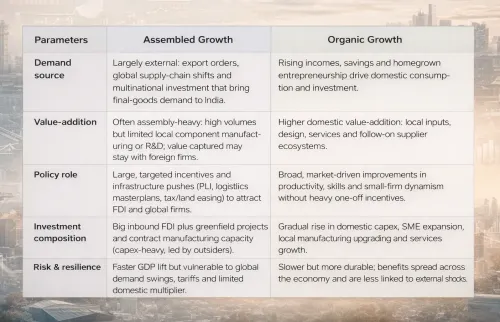

Assembled Growth, Not the Homegrown Kind

Pause here and separate the two kinds of growth that are often mistaken:

Factories, Shops, and Screens: Sectoral Ripples

Manufacturing has been lively.

Index of Industrial Production (IIP) data shows an 8.0% year-on-year expansion in November 2025, led by basic metals, fabricated metal products, pharmaceuticals, and motor vehicles.

This reflects capex and inventory-driven momentum, favouring businesses linked to investment cycles.

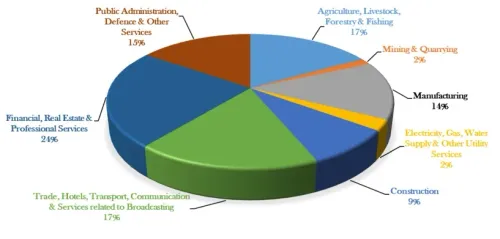

Services remain the heavyweight, contributing around 60% of GVA.

Growth has concentrated in financial, real estate, and professional services, reinforcing the idea that demand is being assembled through finance and services rather than broad household income growth.

Source: Government of India

Retail tells its own story.

Organised retail and e-commerce keep scaling.

India’s e-commerce market was estimated at $53.1 billion in 2024, with double-digit growth projected through 2026.

Scale matters here.

Firms that can source globally and distribute efficiently are winning.

Imports seal the picture.

Non-oil, non-gold imports moved into double-digit growth, touching around $63.6 billion in December 2025.

Demand is strong, but much of it is being met by assembling global inputs locally, rather than replacing imports at home.

The Long View Investors Care About

This is a market-friendly environment, but not a forgiving one.

Debt levels inch up, inequality risks widen, and consumption fatigue lurks if credit tightens or transfers slow.

Wealth and income growth are not missing entirely, but they are not leading the parade.

It is a phase that rewards selectivity more than broad optimism.

Capex, infrastructure, financial services, and organised retail still have visible demand.

Phases like this tend to reward flexibility over fixed narratives.

Credit or consumption shocks can turn sentiment fast.

India’s growth engine is running, no doubt about it.

Just remember, it has been carefully assembled for speed.

Whether it learns to run on its own is a question the economy itself will have to answer over time.

Sources and References:

- ECONOMICTIMES

- PIB

- THEHINDU

- THEHINDUBUSINESSLINE

- VARTHABHARATI

- TRADINGECONOMICS

- OUTLOOKBUSINESS

- WTWCO

- CNBCTV18

- INDIATIMES

- CEICDATA

- CLEARTAX

- GRANTTHORNTON

- MOSPI

- DELOITTE

- IBEF

- ICRA

0 people liked this article.