Welspun Corp (WCL) Q4FY25 Financial Performance: At a Glance

- 2 min read

- 1,075

- Published 18 Dec 2025

Q4FY25 Financial Performance: At a Glance")

Let’s explore the Welspun Corp Q4FY25 results and see how the numbers line up for the coming year. This Q4FY25 financial update sheds light on the key drivers of performance and the outlook ahead.

Revenue and Profit Snapshot

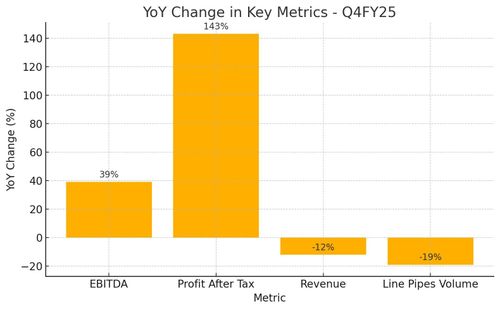

The Welspun Corp Q4FY25 results show that revenue for the quarter came in at ₹3,925 crore, down by 12% from last year. But here’s the interesting part: despite lower revenue, EBITDA jumped to ₹460 crore—up 39% from the same period last year and 6% from the previous quarter. That EBITDA margin improvement is a sign of better control over costs.

Another highlight is the profit after tax, which surged to ₹699 crore—a 143% increase year-on-year. This stands out as a positive in the overall Q4FY25 financial update.

Line Pipes Volume

On the other hand, line pipes volume data showed a decline of about 19% compared to the previous year. This dip is something to watch in future updates, as it could impact operational performance down the line.

FY26 Guidance and Order Book

Now, let’s talk about what’s next. The company has set some ambitious FY26 revenue guidance—₹17,500 crore in revenue and ₹2,200 crore in EBITDA. That’s a big step up from the numbers we’re seeing in this quarter.

Backing up these targets is an order book for FY25 worth around ₹19,553 crore. It’s a good sign that there’s enough work lined up to keep revenue flowing steadily.

Quick Recap Table

Revenue | ₹3,925 crore | -12% |

EBITDA | ₹460 crore | +39% |

Profit After Tax | ₹699 crore | +143% |

Line Pipes Volume | — | -19% |

Here’s what these numbers really say:

-

Revenue and line pipes volume data show some pressure this quarter.

-

But the strong growth in Welspun Corp’s EBITDA and profit after tax tells a story of better cost control.

-

This mixed picture sets the stage for the ADD recommendation and fair value of ₹990.

FY26 Guidance at a Glance

Here’s how the company’s targets for FY26 stack up against Q4FY25:

Revenue | ₹3,925 crore | ₹17,500 crore |

EBITDA | ₹460 crore | ₹2,200 crore |

-

The FY26 targets show a big jump in both revenue and EBITDA compared to this quarter’s numbers.

-

This guidance suggests the company is confident about a strong performance in the coming year.

-

It’s a pretty clear sign that management is focused on scaling up operations and profitability.

Visual Snapshot

To make these changes even easier to see, here’s a quick chart highlighting the year-on-year performance:

Wrapping Up

Overall, while revenue dipped this quarter, the solid improvement in profitability stands out. A healthy order book and a positive outlook for FY26 provide a good sense of stability going forward.

With a fair value of ₹990 and an ADD recommendation, there’s an encouraging tone for the year ahead. It will be interesting to see how the company builds on these numbers.

0 people liked this article.