Kalpataru Projects Q4FY25 Result Update: Strong Performance and Bright Outlook

- 3 min read

- 1,048

- Published 18 Dec 2025

Kalpataru Projects (KPIL) has just announced its Q4FY25 earnings, and the numbers look quite promising. In fact, the company’s performance came in ahead of expectations, signaling continued momentum in the business. Let’s break down the key highlights and what investors can expect going forward.

Q4FY25 Performance Snapshot

KPIL’s Profit After Tax (PAT) for Q4FY25 came in 27% ahead of expectations. This strong showing was driven by a robust ordering environment, especially in the Transmission & Distribution (T&D) and buildings segments.

Here’s a quick look at some of the important financials for Q4FY25:

Standalone Revenue | ₹6200 crore | 21% year-on-year growth, 10% ahead of estimate |

FY25 Order Inflow | ₹25,000 crore | Surpassed guidance of ₹23,000 crore |

Promoter Pledge | 8.2% | Stable sequentially |

The company delivered strong execution aided by steady margin performance, which supported this positive earnings surprise.

What’s Driving Growth?

The ordering environment remains strong, primarily driven by KPIL’s Transmission & Distribution segment and building projects. The opportunity pipeline is also quite healthy:

- Domestic T&D pipeline: ₹60,000 crore annual pipeline for FY25-27

- International T&D pipeline: US $300 million

This solid pipeline underpins the company’s growth prospects and provides visibility for the near future.

FY26 Outlook and Margin Expectations

Looking ahead, KPIL expects FY26 revenue growth of 20% + with a 50 basis points (bps) Profit Before Tax (PBT) margin expansion at the standalone level, and a 100 bps expansion at the consolidated level. The company is also targeting a robust order inflow of ₹26,000 to ₹28,000 crore for FY26.

However, on the consolidated level, the FY26-27 earnings estimates have been trimmed by 13% to 14% due to margin reductions. Despite this, the company remains optimistic about its growth trajectory.

Investment Recommendation

We have retained a BUY rating on Kalpataru Projects with a revised Fair Value (FV) of ₹1,220 as they roll forward to March 2027 estimates. Given the current market price of ₹1,116, this suggests an upside potential for investors over the medium term.

Key Positives and Negatives

Positives:

-

Standalone revenues at ₹6200 crore, beating estimates by 10%

-

Strong order inflow at ₹25,000 crore for FY25, surpassing guidance

-

Healthy opportunity pipeline domestically and internationally

-

Steady margin performance aiding earnings surprise

Negatives:

- Promoter pledge stable at 8.2%, which might raise concerns for some investors

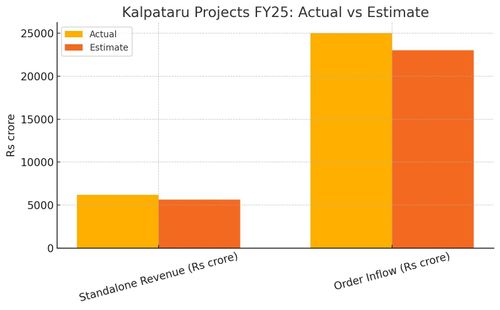

Visualising the Financial Highlights:

Here’s a simple bar chart summarising KPIL’s FY25 key financial metrics versus estimates:

Standalone Revenue | 6,200 | 5,640 |

Order Inflow | 25,000 | 23,000 |

What This Means for Investors

The upbeat Q4FY25 results and a strong FY26 outlook underline KPIL’s operational strength and market positioning, especially in the T&D sector which is critical for India’s infrastructure development.

While the promoter pledge stability might be a concern for some, the overall fundamentals including order pipeline, revenue growth, and margin expansion prospects support a positive investment thesis.

Summary Table: KPIL Q4FY25 Earnings Update

PAT Surprise | 27% ahead of expectations |

Revenue Growth | 21% YoY standalone revenue growth |

Order Inflow FY25 | ₹25,000 crore (above guidance of ₹23,000 cr) |

Margin Outlook | 50 bps PBT margin expansion standalone FY26 |

Opportunity Pipeline | Domestic T&D ₹60,000 cr; International T&D US $300 million |

Promoter Pledge | Stable at 8.2% |

Investment Rating | BUY with FV ₹1,220 |

Kalpataru Projects is shaping up as a solid contender in infrastructure with a strong financial foundation and growth opportunities ahead. For investors looking to capitalise on India’s infrastructure boom, KPIL remains a stock worth watching closely.

If you want to dive deeper, you can always check the detailed Kotak Neo report. But from what we see now, the fundamentals are definitely encouraging for the medium-term investor.

0 people liked this article.