Hindalco Industries Q4FY25 Results: What You Need to Know

- 3 min read

- 1,036

- Published 18 Dec 2025

Hindalco Industries just announced their Q4FY25 results, and there are some interesting highlights worth noting. The company’s earnings before interest, taxes, depreciation, and amortisation (EBITDA) came in ahead of what many expected, mainly thanks to lower coal costs and a stronger showing from their downstream business in India.

Let’s break down what happened and what it means.

Solid Growth in India and Aluminum

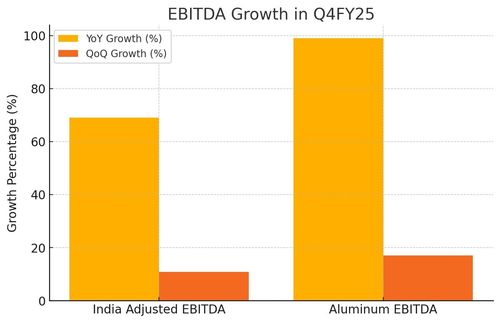

First up, the India business performed really well. The adjusted EBITDA hit ₹5,350 crore in the quarter. That’s a solid jump of 69% compared to the same quarter last year and an increase of 10.8% compared to the previous quarter.

The aluminum segment was particularly impressive. Aluminum EBITDA almost doubled year-on-year, coming in at ₹4,740 crore—a 99% rise from last year and 17% higher than last quarter.

Here’s a quick table to put these numbers in perspective:

India Adjusted EBITDA | 5,350 | +69% | +10.8% |

Aluminum EBITDA | 4,740 | +99% | +17% |

Clearly, the India aluminum division and Novelis were the big contributors to this strong performance.

What’s Happening with the Bandha Mine and Spending?

Looking ahead, the company expects the Bandha mine to start ramping up by the end of FY28. This should add to their raw material supply and support growth. On the spending front, Hindalco is planning to increase capital expenditure, especially in the India business. Despite this, they expect their leverage ratio (a measure of debt compared to earnings) to stay comfortable, which means they are managing their finances prudently.

Here’s a quick summary:

Bandha Mine Ramp-up | Expected by end-FY28 |

Capital Expenditure (Capex) | Set to rise in India business |

Leverage Ratio | Expected to remain comfortable |

What About Copper?

While aluminum saw strong growth, copper EBITDA is expected to remain stable from FY26 through FY28.

Challenges Ahead

It’s not all smooth sailing, though. The company notes that commodity prices remain muted, and there are macroeconomic challenges that could keep earnings relatively flat in the near term.

Market Price and Valuation

As of 21 May 2025, Hindalco’s stock is priced at ₹663. The revised fair value target is ₹735, indicating some upside based on current earnings and outlook.

Current Market Price | 663 |

Fair Value Target | 735 |

Visualising the Earnings Growth

Here’s a clear look at how EBITDA has grown in Q4FY25, both year-on-year and quarter-on-quarter:

What’s Driving Margins?

A few factors helped improve margins in the India business:

Lower Coal Costs | Helped reduce expenses |

Higher Downstream | Increased contribution to profits |

Increased Capex | Supporting future growth |

In Summary

Hindalco Industries had a strong quarter, led by a sharp rise in earnings from their India aluminum business and Novelis. The Bandha mine ramp-up and increased investment in India show the company is focused on growth. Copper earnings should remain steady. That said, softer commodity prices and economic challenges may keep earnings growth modest in the near term.

The company’s financial health looks solid, with manageable debt even as spending increases.

0 people liked this article.