Why Foreign Money Just Poured Into Indian Bonds

- 9 min read

- 13,787

- Published 03 Jul 2026

Some stories arrive with a number so large that the number becomes the story.

₹39,640 crore.

For a few days, every financial newspaper seemed fascinated by it.

Television anchors spoke of it with the excitement usually reserved for election results or record-breaking IPOs.

Foreign investors had poured a record ₹39,640 crore into Indian government bonds in June 2026, comfortably eclipsing the previous monthly record of ₹22,005 crore set in August 2024.

The rupee responded, bond yields responded, and markets responded.

Everyone applauded the number. Not enough people paused to ask why.

Because the funny thing about global money is that it rarely wakes up one morning, stretches, looks at the map, points at India and says, “Today feels like a good day.”

Global capital is far less emotional than that.

It is painfully practical, and it does not reward charm.

It rewards convenience.

Sometimes, it rewards the removal of inconvenience.

That is exactly what happened this June.

It’s not that India has suddenly become irresistible.

It’s that India has quietly removed a hurdle it had placed in front of investors years ago.

Three weeks later, foreign money walked straight through the door.

Sometimes, the biggest market rally begins with someone deciding to stop making visitors fill out unnecessary paperwork.

Source: Press Information Bureau

India’s biggest market had one problem

India has never had a small government bond market; quite the opposite.

By FY26, the outstanding stock of Central Government securities had crossed ₹112 lakh crore, making it one of the largest local currency sovereign debt markets anywhere in the world.

Roads, railways, hospitals, subsidies, salaries, infrastructure, welfare programmes. Governments do not simply wish these into existence.

They borrow, and government bonds are how that borrowing happens.

For decades, the buyers were largely familiar faces.

They were banks, insurance companies, and provident funds.

Domestic institutions that have always formed the backbone of India’s sovereign debt market.

Foreign investors were technically welcome; they simply did not feel particularly invited. That distinction matters.

Before the Reserve Bank of India introduced the Fully Accessible Route, or FAR, in 2020, foreign ownership of Indian government securities generally remained below 2% of the outstanding market.

Put simply, FAR is a set of government bonds foreigners can buy freely, without the investment limits that once made participation feel like more trouble than it was worth.

Compare that with several other emerging economies, where overseas participation has historically been much higher, and the difference becomes difficult to ignore.

India had scale, India had macroeconomic credibility, and India had growing global relevance.

What India also had was a collection of small irritants that, when added together, became one very large deterrent.

Investment limits on several securities, registration requirements, settlement infrastructure that looked rather different from what global funds were used to, and operational complexity.

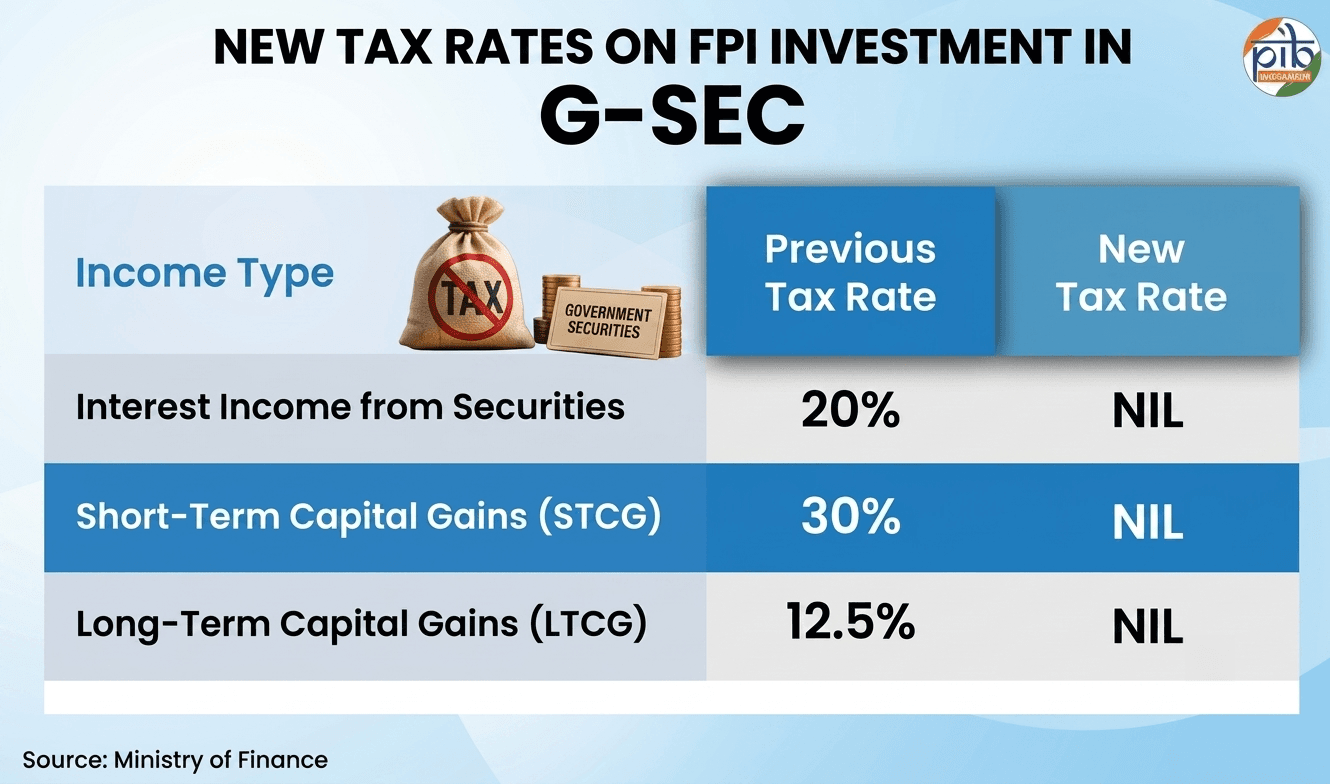

What more? A tax on interest income earned from government bonds, and another tax on capital gains.

None of these hurdles was individually catastrophic.

Together, however, they created something that institutional investors dislike far more than volatility.

Friction.

And when a fund manager is allocating money across 30 countries before lunch, friction often loses to simplicity.

One ordinance changed everything

There is something oddly satisfying about watching years of market behaviour change because of a few carefully chosen lines in a legal document.

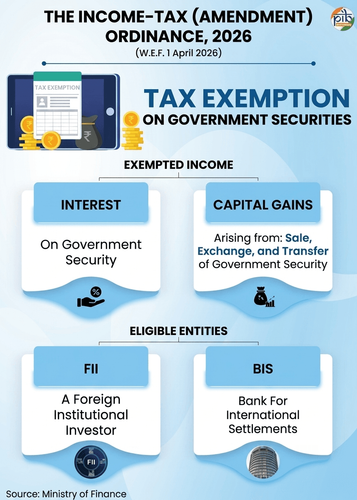

On 5 June 2026, the government promulgated the Income-tax (Amendment) Ordinance, 2026.

It sounded technical. It turned out to be transformational.

Imagine budgeting every year for a tax you had always paid, then discovering it had simply gone.

That is roughly what happened for many foreign bond investors.

For those using the Fully Accessible Route, the government removed the withholding tax on their interest income, close to a fifth of what they earned, and lifted the tax on their long-term capital gains as well.

Better still, the change applied retrospectively from 1 April 2026.

Source: Press Information Bureau

The Reserve Bank of India happened to make life even more interesting around the same time by expanding the Fully Accessible Route to include 30-year government securities.

That seemingly modest decision opened another door.

Long-duration bonds are particularly attractive for pension funds and insurance companies because their liabilities stretch across decades.

Matching long-term obligations with long-term assets is hardly the sort of thing that dominates dinner-table conversations, but it matters enormously to institutional investors managing billions of dollars.

Suddenly, India was offering exactly the sort of maturity profile these investors preferred. The response was immediate.

According to CCIL data, foreign holdings of these bonds rose by roughly ₹35,000 crore in the three weeks that followed.

By the end of June, total inflows had reached the now-famous ₹39,640 crore.

It was not merely another good month.

It became the strongest month foreign investors had ever had in India’s government bond market.

The timing tells its own story.

Money was not waiting for India to become economically stronger overnight.

It was waiting for India to become operationally easier.

When money follows the index

Passive investing is always amusing.

Imagine managing billions of dollars while making remarkably few decisions.

That is essentially what passive funds do.

They are not trying to outsmart the market.

They are not attempting to predict elections, inflation, central bank meetings or exchange rates.

Their job is wonderfully uncomplicated.

Follow the index.

If the index includes a country’s government bonds, they buy them.

If the country’s weight increases, they buy more.

If the country leaves the index, they sell.

No drama. No debates. No opinion.

Just plain simple mathematics.

India experienced this first-hand when its inclusion in the JPMorgan Government Bond Index Emerging Markets Global Diversified Index began in June 2024 and concluded in March 2025.

By the end of the phased inclusion, India had reached the maximum permitted weight of 10%.

That seemingly administrative development quietly brought an estimated US$20 billion to US$25 billion of passive foreign capital into Indian government bonds over roughly 10 months.

Source: Business Standard

Not because thousands of portfolio managers independently concluded India was their favourite destination.

Because the benchmark instructed them to own India.

That distinction is one every investor should remember.

Markets often celebrate foreign inflows as a vote of confidence.

Sometimes they are; sometimes they are just a consequence of how global indices work.

And understanding that difference helps explain why another index has become the next big prize.

While India has already earned its place in JPMorgan’s emerging market benchmark, an even larger audience is still waiting outside the door.

The Bloomberg Global Aggregate Bond Index.

Source: Business Standard

This is where the picture begins to stretch well beyond one extraordinary month of inflows and starts becoming something equity investors should pay very close attention to.

Because the next chapter is not really about bonds,

It is about borrowing costs, banks, home loans, and the rupee in your wallet.

And, perhaps surprisingly, it is also about the stocks sitting quietly inside your portfolio.

If JPMorgan opened one highway into India, Bloomberg could open another.

The travellers look different: broader, deeper, less emerging-market in flavour.

But the logic is the same.

Money that arrives not because it admires the destination, but because an index requires it to.

The bigger prize ahead

The June record may have dominated headlines, but it is unlikely to be the biggest story of the year.

That honour could belong to the Bloomberg Global Aggregate Bond Index.

India has been working towards inclusion for over a decade, but Bloomberg deferred its decision in January 2026, citing settlement infrastructure, post-trade processes and taxation.

The June ordinance removed one of those hurdles by exempting eligible FPIs from tax on interest income and capital gains, strengthening India’s case further.

If India secures an estimated 1% weight in the index, analysts expect another US$20-22 billion of passive inflows over 10 to 12 months.

Unlike active investors, index funds do not wait for the perfect macro environment.

They buy because the benchmark tells them to.

The ripple effect begins

Foreign investors buying government bonds push prices higher and yields lower.

Since the June policy measures, the benchmark 10-year government bond yield has eased by around 20 basis points to 6.76%.

That matters because government bond yields rarely stay confined to the debt market.

They influence borrowing costs across the financial system, making them an important benchmark for banks, businesses and housing finance companies.

Combined with the RBI’s two rate cuts this year, lower yields point towards a more supportive borrowing environment.

The connection may not be obvious, but it is real.

A foreign fund buying a 30-year government bond today can eventually influence the EMI a household pays tomorrow.

The rupee joins the rally

Bond inflows also created fresh demand for the rupee.

After slipping to a record low of around ₹97 against the US dollar in late May, the rupee staged a sharp recovery through June, ending the quarter near ₹94.7.

Easing oil prices and policy measures to attract foreign capital helped improve sentiment and supported the currency’s rebound.

A stronger rupee helps moderate the cost of imported crude oil, edible oils, electronics, machinery and industrial components, easing inflationary pressure across the economy.

Importers stand to benefit, while exporters with significant dollar revenues could face some near-term pressure.

Where investors may look next

For equity investors, this is less about one record month and more about the sectors that could benefit if foreign participation becomes structural.

Banks such as HDFC Bank, State Bank of India and Kotak Mahindra Bank could gain from stronger treasury portfolios and lower funding costs as yields soften.

Housing finance companies, including LIC Housing Finance and Can Fin Homes, could benefit if lower long-term yields improve funding conditions and support home loan affordability over the next 12 to 18 months.

The bigger takeaway is to distinguish between active and passive foreign money.

June’s record inflow reflected active investors responding to a more favourable tax regime.

Passive capital is different.

It arrives because a benchmark demands it and usually stays for much longer.

That is why the Bloomberg Global Aggregate Bond Index matters far more than the ₹39,640 crore headline.

Countries often spend years trying to convince global investors to believe in them.

India may have discovered that belief is only part of the equation.

Sometimes capital does not ask whether a country is promising. It asks whether participating is easy.

June's record inflow may therefore be remembered less as the month foreign investors discovered India, and more as the month India finally removed enough friction for global capital to behave exactly as it always does.

Sources and References:

- OUTLOOKBUSINESS

- PIB

- SSGA

- NEWSINDIANEXPRESS

- SWARAJYAMAG

- BUSINESSSTANDARD

- MONEYCONTROL

- LIVEMINT

- TIMESOFINDIA

- REUTERS

This article is for informational purposes only and does not constitute financial advice. It is not produced by the desk of the Kotak Securities Research Team, nor is it a report published by the Kotak Securities Research Team. The information presented is compiled from several secondary sources available on the internet and may change over time. Investors should conduct their own research and consult with financial professionals before making any investment decisions. The above images were generated using AI. Read the full disclaimer here.

Investments in securities market are subject to market risks, read all the related documents carefully before investing. Brokerage will not exceed SEBI prescribed limit. The securities are quoted as an example and not as a recommendation. SEBI Registration No-INZ000200137 Member Id NSE-08081; BSE-673; MSE-1024, MCX-56285, NCDEX-1262.

0 people liked this article.