India’s Family Business Reset

- 4 min read

- 5,466

- Published 22 May 2026

If you have grown up around Indian family businesses, you know the scene.

The founder sits at the head of the table, the balance sheet in one hand and a lifetime of risk in the other.

The children sit politely, educated abroad, ambitious in their own way, but not always interested in inheriting the factory, the dealership, the hospital chain.

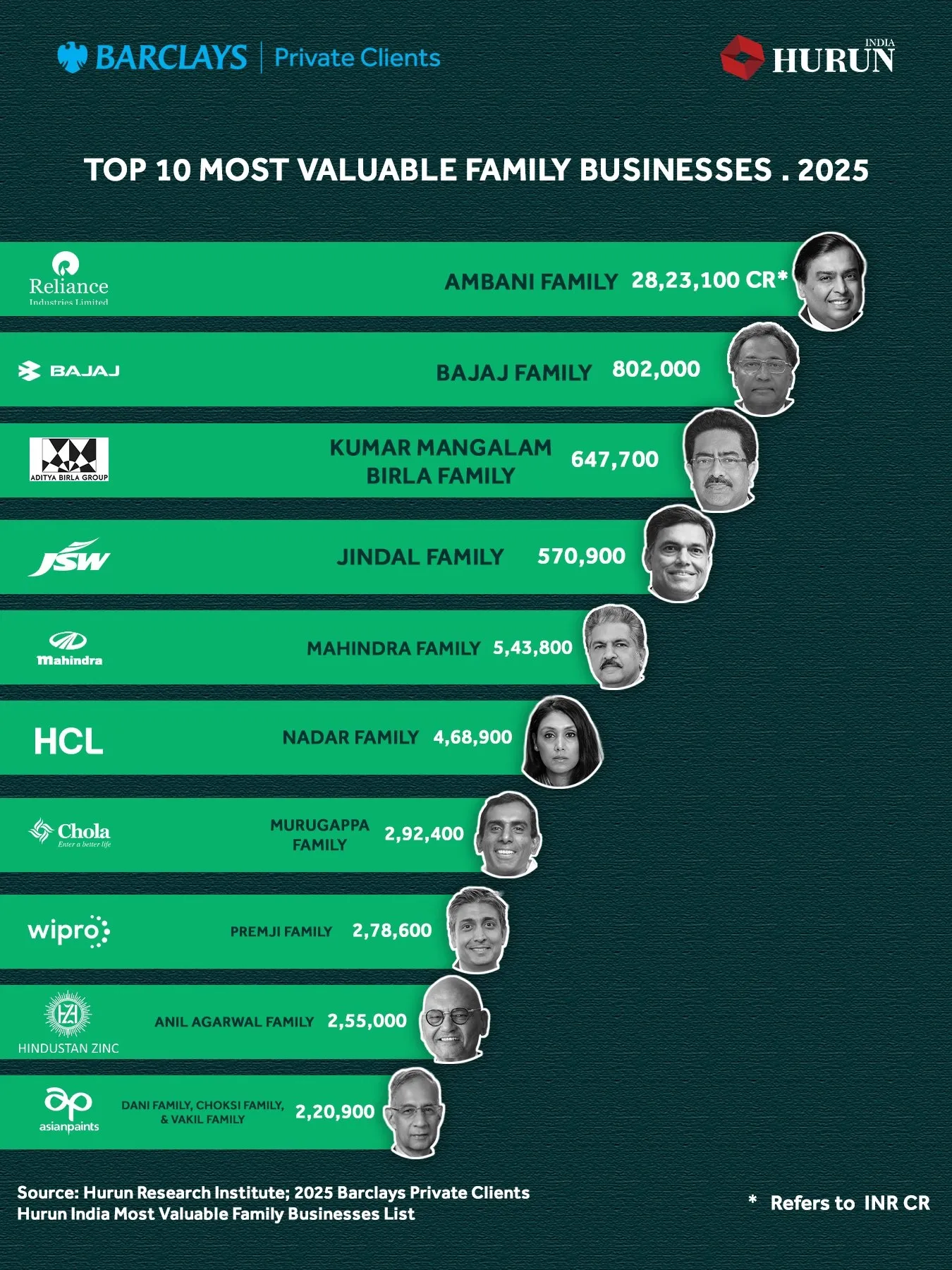

The family silver is valuable.

The question is, who wants to polish it?

Now stretch that dining table across the country.

Multiply that quiet hesitation by thousands of boardrooms.

What looks like a family conversation is slowly becoming an economic event.

India is staring at one of the largest intergenerational wealth transfers in its history.

As of 2024, around 70% of India’s 334 billionaires are expected to pass on roughly $1.5 trillion to the next generation.

That figure alone accounts for over one-third of GDP.

It sounds majestic. It is also slightly unsettling.

Because nearly 36% of Indian family businesses still do not have a clear succession plan.

About 52% say resistance from the senior generation is the biggest barrier to transition.

Another 21% admit they are simply delaying the inevitable due to uncertainty.

And while 79% of founders intend to pass their businesses to family members, 45% do not actually expect their children to take over.

Only 17% of heirs feel obligated to join the family enterprise.

This is not just family drama.

It is the capital waiting for direction.

And capital, when left waiting, rarely stays idle for long.

Source: Forbes India

Liberalisation’s Children Are Now Retiring

Many of these businesses were born in the 1990s, in the glow of economic reforms.

First-generation entrepreneurs built factories, distribution networks, real estate portfolios and regional brands from scratch.

Three decades later, a large cohort of them is approaching retirement at the same time. That simultaneity matters.

When an entire generation of founders begins to step back, valuations, ownership structures and governance models start shifting together.

Some businesses will professionalise.

Some will seek partial exits.

Some will quietly look for buyers.

And some will struggle because there is no clear handover plan.

For stock traders and investors, this is not sentimental. It is structural.

Meanwhile, Private Equity Is Restless

While promoters contemplate succession, private equity firms are sitting on about $2.18 to $2.2 trillion in dry powder globally.

Even after easing from the 2023 peak of $2.3 trillion, this remains historically elevated.

Over 40% of that capital has been ageing for more than two years.

Money that does not get deployed starts feeling impatient.

In 2025, dealmaking returned with force.

Global private equity deal value rose to $2.1 trillion, up from $1.8 trillion in 2024.

Buyout and growth deals above $500 million surged 44% to cross $1 trillion, the highest on record.

Exits jumped more than 40%, with IPO-led exits nearly doubling, restoring liquidity to the ecosystem.

That liquidity is oxygen.

It encourages new bets.

Yet overall deal counts remain subdued, reflecting selectivity and valuation discipline.

Which means mid-sized, promoter-led firms with stable cash flows suddenly look attractive.

They are large enough to matter.

Small enough to negotiate.

And often at valuations that are less inflated than megadeals.

If you are an investor watching 2026 unfold, this is where the action quietly builds.

The Family Office Awakening

There is another player at the table now.

The family office.

India has about 300 family offices today, up from just 45 in 2018.

Together, they manage roughly $30 billion in assets under management, projected to rise to $45 billion within three years.

That implies 50% growth and a 14% CAGR.

Globally, family offices oversee more than $6 trillion.

India is early in the curve, but the slope is steep.

These are no longer informal pools parked in fixed deposits and real estate.

While 57% still allocate under 10% to private equity and venture capital, allocations are rising.

Families are diversifying into private equity, private credit, venture capital and global equities.

Alternative investments are expected to grow faster than traditional ones, with AIF exposure alone projected to rise by 5% over the next three years.

Governance is maturing, too.

About 59% of Indian families now have wills or constitutions in place, and 19% use trusts or LLP structures.

The shift from promoter instinct to institutional framework is underway.

Capital is not just available.

It is becoming structured, patient and increasingly strategic.

Source: The Indian Express

Growth Is Still Strong

Here is the part that makes the convergence even more interesting.

These are not distressed businesses.

Around 63% of Indian family businesses recorded double-digit revenue growth in 2024.

75% are targeting over 15% growth by 2025 to 2026.

89% plan to expand within Asia-Pacific.

40% are eyeing North America and Europe.

53% already use AI to improve margins and scalability.

17% are engaging with private equity.

15% are planning IPOs.

Put all these strands together and a pattern begins to form.

Founder-led companies are still expanding aggressively.

Families reorganising their own wealth.

This is not decline. It is transition.

Where the Shifts Will Be Visible

Look at MSMEs and traditional manufacturing first.

Many are family-run and face credit gaps.

Succession uncertainty makes lenders cautious, increasing reliance on private equity or strategic investors.

Consolidation is likely. Roll-ups will appear.

Real estate and construction follow close behind.

These assets often sit within family portfolios and depend on relationships.

Leadership transitions can stall projects or unlock joint ventures with institutional capital.

Consumer and retail businesses are ripe for reinvention.

Regional FMCG brands and legacy retail chains face generational strategy shifts.

The next generation prefers digital channels and brand repositioning.

Capital providers see scaling opportunities.

Healthcare and education enterprises, often promoter-led, depend heavily on founder reputation.

Succession gaps can expose operational fragility.

Professional management backed by institutional capital can trigger rerating.

If you are scanning mid-cap screens in 2026, look for subtle signals.

A professional CEO appointment.

A private equity stake sale.

Governance reforms.

These often precede valuation shifts.

The Market Angle

This is not a nostalgic story about founders retiring. It is a capital cycle.

Mid-sized companies undergoing generational transitions can become acquisition targets, consolidation plays or IPO candidates.

Firms with clear succession plans, strong cash flows and institutional interest may see reratings.

Those with promoter disputes or opaque structures may see the opposite.

Governance clarity might matter as much as earnings growth in this phase.

When succession anxiety meets record capital availability, price discovery accelerates.

Some family businesses will find strategic partners.

Some will partially exit at peak valuations.

Some will reinvent themselves under professional management.

For investors and traders positioning for 2026, the opportunity is not in guessing which founder retires next.

It is in identifying which businesses are prepared sellers and which funds are disciplined buyers.

The dining table conversation is moving to the boardroom.

And capital is already waiting at the door.

Sources and References:

- TIMESOFINDIA

- FORBESINDIA

- OUTLOOKMONEY

- SPGLOBAL

- MCKINSEY

- KPMG

- BUSINESSSTANDARD

- EY

- INDIANEXPRESS

- DELOITTE

The content in this blog is intended purely for educational purposes. Any securities or mutual funds referenced are illustrative in nature and do not constitute a recommendation or endorsement by Kotak Neo. Investors are encouraged to assess their own financial situation and seek professional advice before making any investment decisions. For compliance T&C and disclaimers, Visit https://www.kotakneo.com/disclaimer/

0 people liked this article.