Commodities Research - Base Metals Weekly

- 6 min

- 1,056

- Published 19 Oct 2023

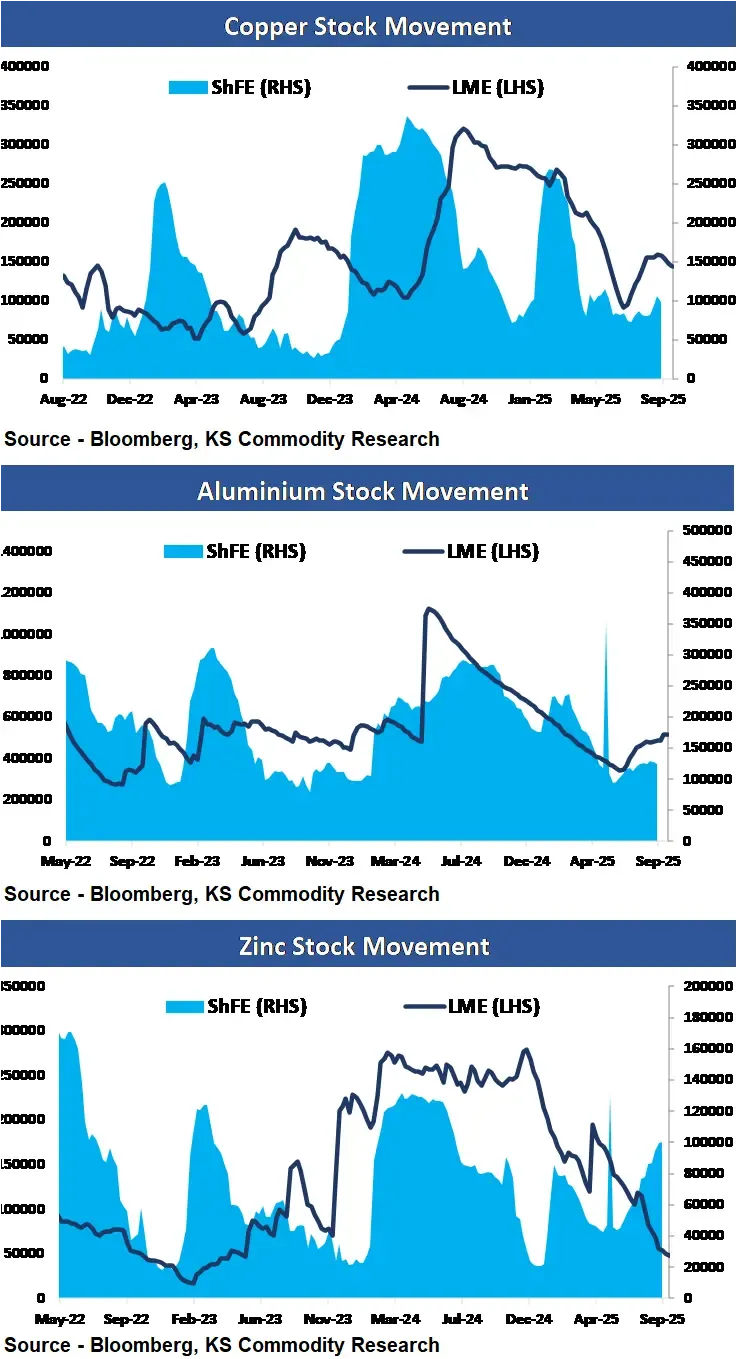

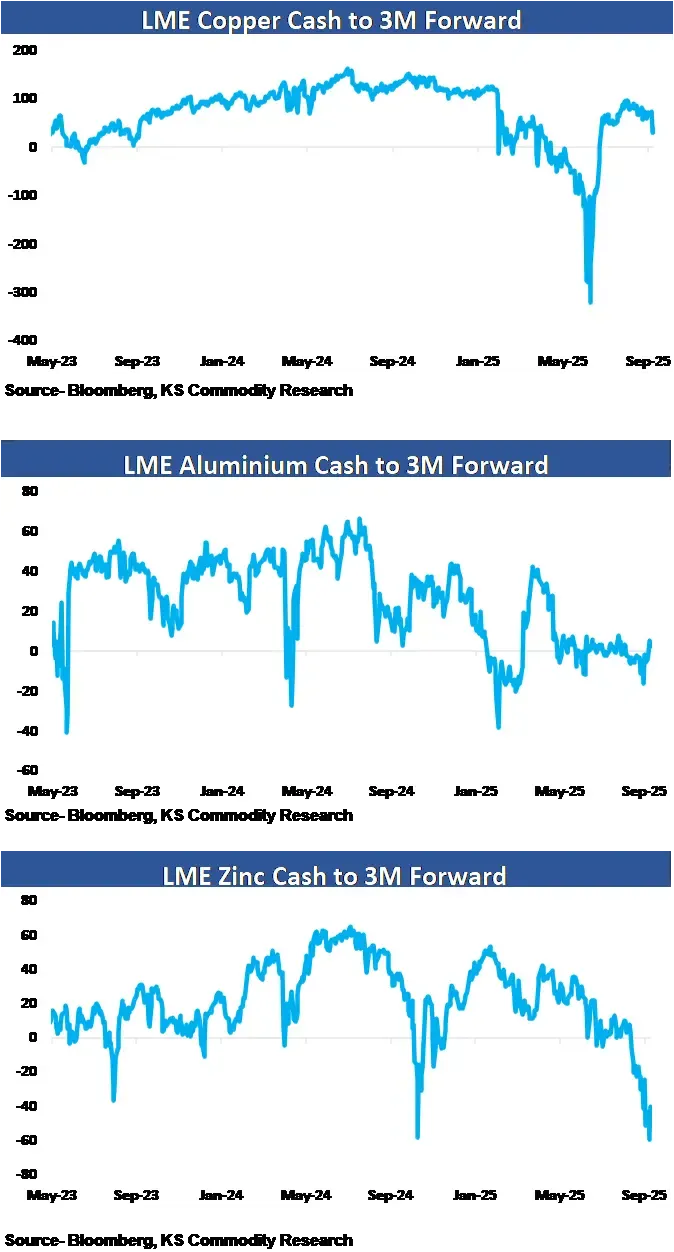

Copper – Copper prices extended strong gains over the past week, with LME copper rising nearly 2% to close above $10,181/ton, while MCX copper advanced over 3%, settling above ₹9,936/kg, reaching multi-month highs. The rally was largely driven by significant supply disruptions at major operations. Freeport-McMoRan’s Grasberg mine in Indonesia remains under force majeure following a deadly mudflow earlier in September. Considering that this single mine accounts for over 3% of global copper production, it highlights the market’s sensitivity to supply disruptions. Similarly, another mine, Constancia in Peru halted production amid local protests, while Chile’s Codelco indicated that its El Teniente mine may take longer than anticipated to return to full capacity, contributing to an estimated 33,000-ton shortfall this year. On the demand side, Chinese smelters called for stricter control over new capacity as cut-throat competition pushed processing fees to record lows, while restocking ahead of China’s Golden Week provided seasonal support. However, gains were partly capped by a firmer US dollar, supported by stronger-than-expected GDP growth, which tempered expectations of aggressive Fed rate cuts, coupled with softening margins at Chinese smelters also weighed on sentiment. Copper is expected to remain supported this week by persistent supply constraints and solid Chinese demand in the run-up to Golden Week, reinforced by Beijing’s efforts to boost supply and back its new-technology and EV sectors. Even so, broader macro headwinds and a stronger dollar could limit additional gains. Trading range for the week is 930 - 981

Aluminium - Aluminium prices extended their recent pullback last week, with MCX aluminium slipping nearly 2% to close above ₹255/kg, while LME aluminium settled at $2,655/ton. The global bauxite market in H1 2025 showed a mixed picture. Leading producers such as Guinea and Australia benefited from strong Chinese demand and stable supply chains, whereas Turkey and Brazil lagged behind. Guinea, the world’s largest supplier, shipped around 99.8 million tonnes in the first half of the year, a 36% rise from 2024, with China accounting for roughly 60% of exports. This robust Chinese demand also drove a 4% increase in aluminium output by domestic smelters during the first five months of the year. Aluminium production remained steady in August, averaging 202,500 tons per day, while LME inventories inched up to 517,700 tonnes. In North America, demand fell 4.4% year-on-year in H1 2025, pressured by tariffs and weaker exports. US business activity moderated in September, with PMI surveys signaling slower growth across manufacturing and services, though GDP revisions showed a 3.8% expansion in Q2. Looking ahead, aluminium is expected to trade within a range, underpinned by tight supply and sustained Chinese demand. Contained inflation has kept the Federal Reserve on track for potential rate cuts, providing some support, although mixed US economic data and any uptick in the dollar may temper further upside. Trading range for the week is 251 - 268

On the daily chart, MCX Copper has breached out of the key resistance of the ascending triangle pattern. The price is sustaining above the 20-days moving average, further re-enforcing the bullish trend. The momentum indicator RSI (14) has crossed above the 60 mark which further confirms the bullish momentum. These signals point towards a strong bullish bias in the near term. Immediate resistance is placed at 964, followed by 981, while on the downside, support is seen at 931 and the next key level at 910. Based on the current setup, MCX Copper Futures are expected to trade within the 930–981 range in the near term, with a sideways to bullish bias.

On the daily chart, MCX Aluminium are currently following an upward parallel channel, indicating that the bullish structure remains intact. The price is hovering above the 20-days moving average, further reinforcing the ongoing bullish sentiment. Additionally, the RSI continues to trade above the 50 mark, suggesting sustained momentum on the upside. Immediate support is seen at 251, followed by the critical support at 246. On the upside, immediate resistance is placed at 262, with a stronger resistance level at 268. Based on the current setup, the price is expected to trade within the 251–268 range in the near term, with a sideways to bullish bias.

BUY | We expect the commodity to deliver 2% or more returns. |

SELL | We expect the commodity to deliver (-2%) or more returns. |

SIDEWAYS | We expect the commodity to trade in the range of (+/-) 2%. |

Anindya Banerjee | |

Kaynat Chainwala | |

Riteshkumar Sahu | |

Saish Sawant Dessai |

Abhijit Chavan | Jimesh Chauhan | Durgesh Ugawekar | Nikesh Kumar | Gyan Singh |

The content in this blog is intended purely for educational purposes. Any securities or mutual funds referenced are illustrative in nature and do not constitute a recommendation or endorsement by Kotak Neo. Investors are encouraged to assess their own financial situation and seek professional advice before making any investment decisions. For compliance T&C and disclaimers, Visit https://www.kotakneo.com/disclaimer/

0 people liked this article.